Secondaries transactions in the funds sector

Secondary transactions offer liquidity and flexibility to the funds sector.

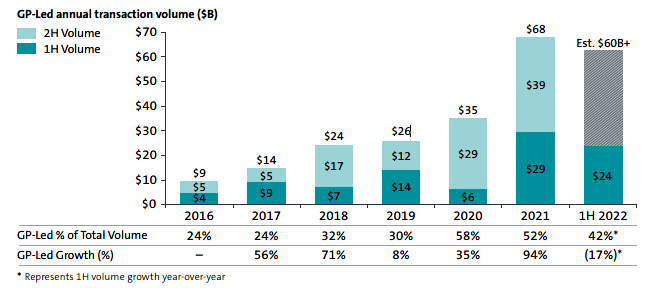

Secondaries led by general partners (GPs) have become an integral feature of the fund secondaries market. In the first half of 2022, they represented 42% of all secondary transactions, compared with 24% in 20171.

What’s more, many believe the GP-led segment of the market is poised for further growth and is likely to exceed US$200 billion by 20252.

A GP-led secondary transaction comes in many forms. The main options are as follows:

However, common to all structures is the fact that a secondary buyer acquires existing investments. These will often reside in a new holding vehicle.

The motivations and incentives for sponsors and investors of GP-led secondary transactions include the following:

The Net Asset Value (NAV) of the assets being transferred is often historical, having been set at the outset of the deal. The deal may take a considerable time to complete. If the relevant market is moving upwards during this period, the NAV may look conservative by the time the deal closes. Commentators have pointed out that this arrangement favours new investors but the issue of fair pricing can be addressed using various strategies (see “Stumbling blocks and how to navigate them” below).

The costs of the transaction will not be met by the GP. Instead, often the sale costs will be paid by the main fund, with the costs of setting up the continuation fund being met by both new investors and rolling investors.

GP-led secondary funds tend to have lower management fees than primary funds. So, while a smaller private equity fund might have a management fee of, say, 2% p.a. of committed capital, the figure for a GP-led secondary fund might be, say, 0.5% to 1.25% p.a. of drawn capital. Inevitably, the negotiated figure will depend on the particular circumstances of the transaction, including the size of the fund and the expected role of the fund manager in the further development of the investment, as well as market practice generally.

New investors will want to see that the GP continues to have “skin in the game”, for example by reinvesting any carried interest and GP commitment received on the sale into the new vehicle. In practice, a rollover of crystallised carry may mean a very significant commitment on the part of the GP, well in excess of its original investment.

The carried interest percentage may also be lower than the usual 20%, although it may ratchet upwards on a performance-related basis. There may also be a higher hurdle to overcome before the GP can begin to receive carried interest.

Rollover investors will look carefully at their tax positions. The deal may be structured to ensure that no tax loss or gain is crystallised, and the original cost basis is retained. This is known as a “tax-free roll”. An “after-tax roll” is an alternative structure, where the rollover amount is net of any tax withheld or payable.

Investors in primary funds who are faced with the option to exit or roll over have voiced concerns regarding GP-led secondaries. These focus on three main areas: pricing; timing; and conflicts. However, given the stability of the secondaries market, reflected in the increasing number of high-calibre players and the sheer volume of secondary transactions in recent times, these concerns can be overstated. To navigate them, it makes sense for GPs to engage with the fund’s Limited Partner Advisory Committee (LPAC) as early as possible in the process.

Regarding pricing: existing investors contemplating an exit will be keen to ensure that the assets being acquired by the secondary vehicle are priced fairly, in the absence of an exit mechanism such as an open market sale or IPO. This is especially so with stapled secondaries, where new investors will be contributing capital to a new fund managed by the GP, as well as participating in its secondary vehicle.

GPs seeking consensus on pricing would be well advised to provide details of relevant valuations, financial models and projections to the LPAC for wider dissemination. If there has been a bidding process, giving an overview of bids received might also be helpful. Additionally, the guidance released by the Institutional Limited Partners Association (the ILPA Guidance) suggests that, in complex restructurings, a fairness opinion from an independent financial consultant might also provide reassurance.

Regarding timing: tight timeframes and momentum on these transactions are important.

It would be sensible for GPs to communicate the rationale for the transaction, the process and the projected timings to the LPAC as soon as practicable. The ILPA Guidance suggests that the GP might consider engaging a secondaries adviser to support the process and to assist in communicating information to investors (eg in relation to any bids received). In terms of a concrete time frame, the ILPA Guidance recommends 20 business days for existing investors to evaluate the sale/purchase information and to make their choice.

Regarding conflicts of interest: these will arise among existing investors, new investors and the GP. This is especially so where new investors are offered different terms from those offered to rollover investors. There should be detailed disclosures to investors regarding these issues; attempts to mitigate conflicts should be considered and, where possible, made; and any conflicts should be approved by the fund’s LPAC or otherwise appropriately approved in accordance with the fund’s constitutional documents.

The market view has developed in recent years in relation to GP-led secondary transactions. Gone are the days when a continuation fund was viewed solely as a way to simply “move” unrealised portfolio investments out of a fund in distress – struggling to make exits and/or unable to return capital to its investors – or nearing the end of its life.

GP-led secondaries are now increasingly a valuable feature of the investment fund environment, with a dramatic increase in transaction volumes over the last few years. Opting for a GP-led secondary transaction provides fund managers and investors alike with many and various opportunities. Particularly useful is the chance to extend the holding period of the fund’s assets in order to maximise value, as well as to gain added liquidity within a large and maturing market.

1. Jefferies, 1H 2022 Global Secondary Market Review (July 2022).

2. Lazard Private Capital Advisory, Sponsor-led Secondary Market Report 2021 (January 2022).

Authors: Nick Goddard, Partner; Samantha Hedley, Junior Associate; Nikita Pandit, Trainee

The information provided is not intended to be a comprehensive review of all developments in the law and practice, or to cover all aspects of those referred to.

Readers should take legal advice before applying it to specific issues or transactions.