Briefing On EU Carbon Border Adjustment Mechanism and Consultation on UK CBAM

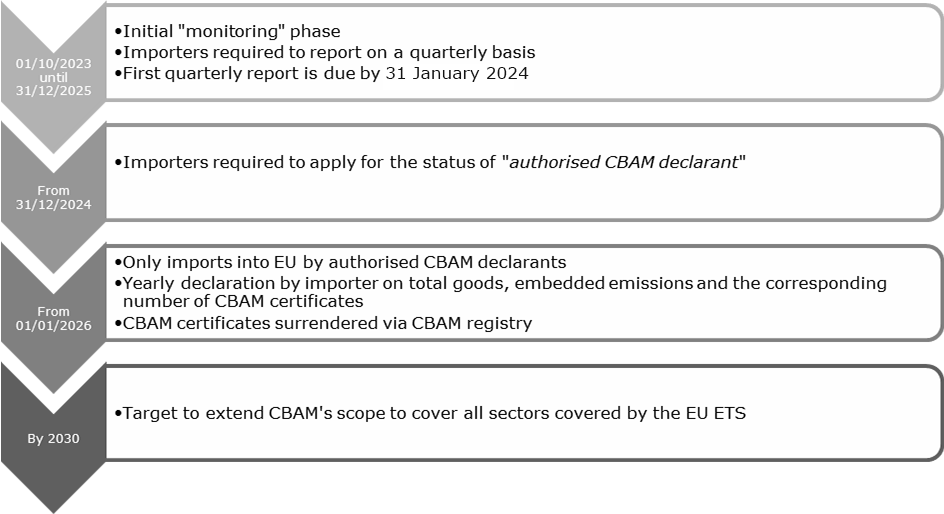

The EU has adopted the world's first Carbon Border Adjustment Mechanism (CBAM) which will have effect from October 2023. Until the end of 2025, importers will be subject to CBAM reporting requirements. CBAM will become fully operational from 2026, requiring importers to pay a carbon import levy for certain "carbon-intensive" goods originating from countries that lack an equivalent carbon pricing regime. The CBAM's main objective is to reduce "carbon leakage" and incentivise the EU's global trading partners to decarbonise their heavy emitting sectors.

The CBAM is one of the key pillars of European climate policy, together with the parallel reform of the EU Emissions Trading System (EU ETS). The plan to introduce CBAM was first announced by the EU in December 2019 as part of the Green Deal, the EU's commitment to be climate-neutral by 2050. In April 2023, both the European Parliament and the Council voted on its adoption. The CBAM Regulation will be published in the Official Journal of the European Union before it enters into force.

Following Brexit, the UK replaced its participation in the EU ETS with the UK Emissions Trading Scheme taking effect from 1 January 2021. In March 2023 British officials indicated that there should be greater cooperation between the UK and EU on carbon leakage in response to the US Inflation Reduction Act, which provides for a $369bn green subsidy programme. The similar designs of the UK and EU emissions trading schemes raises the possibility of formally linking the two, potentially meaning that the UK could be exempt from the EU CBAM. On 30 March 2023, HM Treasury and the Department for Energy Security and Net Zero published a consultation on potential policy measures to mitigate carbon leakage risk and support decarbonisation of UK industry, including proposals for a UK CBAM.

The ETS was introduced in 2005 and has since led to an approximate 40% decrease in EU greenhouse gas emissions in the main industries covered, i.e. power and heat generation, energy-intensive industry and aviation. Under the EU ETS, emitters must either reduce their emissions, or purchase emission allowances on the carbon market at a given carbon price.

The EU ETS works with a mechanism of free allowances for sectors considered to be at high risk of carbon leakage, i.e. EU production moves to non-EU countries with less stringent climate requirements or EU products are replaced by more carbon-intensive imports. This mechanism has attracted criticism over the years as it may disincentivise sectors from taking any long-term action to decarbonise, and will therefore be gradually phased out.

The CBAM is designed to reduce the risk of carbon leakage as free allowances are phased out. The reformed EU ETS will maintain the current mechanism of free allowances. However, from 2026 onwards, and over a period of nine years, this mechanism will gradually be replaced by the CBAM.

The CBAM will introduce a carbon price on emissions embedded in certain goods upon importation into the EU: cement, iron and steel, aluminium, fertilisers, electricity and hydrogen. The scope of CBAM may be further extended after 2026 (e.g. organic chemicals and polymers). The aim is to cover all EU ETS sectors by 2030. Imports from all third countries will be covered, except if expressly excluded in the Regulation, for instance EFTA countries (Iceland, Liechtenstein, Norway and Switzerland).

The visual below summarises the CBAM timeline and implementation requirements:

The sale of CBAM certificates is regulated in Chapter IV of the CBAM Regulation. Member States will sell the certificates to authorised CBAM declarants established in their Member State. The Commission will establish and manage a common central platform for this purpose.

The price of CBAM certificates will calculated on a weekly basis by the Commission, as the average of the closing prices of EU ETS allowances on their designated common auction platform.

The authorised declarant must surrender, through the CBAM registry, the number of certificates corresponding to the embedded emissions declared for the previous calendar year. If a declarant has purchased an excess of certificates, certificates may be re-purchased by the Commission through the common central platform, on behalf of the Member State where the declarant is established, and at the price the declarant originally paid.

Certificates bought by the declarants are stored on the CBAM registry and automatically surrendered to the Commission. The registry will contain data on the authorised CBAM declarants, operators and installations in third countries, which will be available to customs and other competent authorities from Member States.

Information in the registry will not be accessible to the general public, with the exception of the names, addresses and contact details of operators and the location of installations in third countries. However, an operator can opt out of having its information made accessible to the public.

On 30 March 2023, HM Treasury and the Department for Energy Security and Net Zero published a consultation on potential policy measures to mitigate carbon leakage risk and support decarbonisation of UK industry. The consultation is considering policies for mitigating the carbon leakage risk in the following sectors: cement, chemicals, glass, iron and steel, non-ferrous metals, non-metallic minerals, paper and pulp, refining, fertilisers, and power generation.

One of the options that the consultation is exploring is the development of a separate UK CBAM which, just like the EU CBAM, would apply to imported products to ensure they are subject to a comparable carbon price to that incurred by UK-based producers. The consultation timeline indicates the earliest potential introduction of a UK CBAM in a limited number of sectors would be 2026, which is in line with UK ETS reforms on free allowances, and the full implementation of the EU CBAM.

Other options being considered by the consultation include:

The consultation runs until 22 June 2023.

The CBAM has important implications for importers of goods covered by the CBAM as well as for businesses relying on such imports in their supply chain.

It is important that importers who are directly impacted by the CBAM develop a plan to ensure compliance with the requirements (see implementation timetable above), including data collection for reporting purposes, and registration as authorised CBAM declarants.

Depending on the country of origin of imports, the CBAM may give rise to a significant carbon cost for imported CBAM goods when fully introduced. It would therefore be prudent for businesses to map out the potential impact on their key markets and value chains.

We would like to thank Eli Garrett for his assistance with this briefing.

The information provided is not intended to be a comprehensive review of all developments in the law and practice, or to cover all aspects of those referred to.

Readers should take legal advice before applying it to specific issues or transactions.