Changes to providing financial services into the UK may be about to become harder

The FCA has published its periodic Perimeter Report. It sets out financial issues that fall outside its perimeter. It can be summarised as there isn’t a financial issue outside the regulatory perimeter that can't be improved by bringing it within the FCA's oversight.

Of particular interest to international firms providing cross border services to UK clients is the FCA's aim to have more oversight over the overseas persons exclusion (OPE) and a desire to provide greater "clarity" about when a regulated activity is being carried on in the UK.

Although there are no specific recommendations, this could have significant implications for firms providing cross border services into the UK. Firms that provide cross border services into the UK will need to review carefully any proposed changes. Even minor changes to the OPE, which has been in place since the 1980s, could fundamentally change a key part of what makes London a global financial centre.

The FCA has two proposals:

Despite being part of the UK's regime since the 1980s, the OPE, and its role in the UK's liberal regime for the provision of "non-UK- authorised" cross border services, is often misunderstood. In order to fully understand why this matters we have to return to the central concept in the UK financial services regime – the general prohibition. This is something that most people in the financial services industry do not have to think about on a day-to-day basis because they are UK-authorised but it is the reason why everyone from globally systemic banks through to IFAs need authorisation.

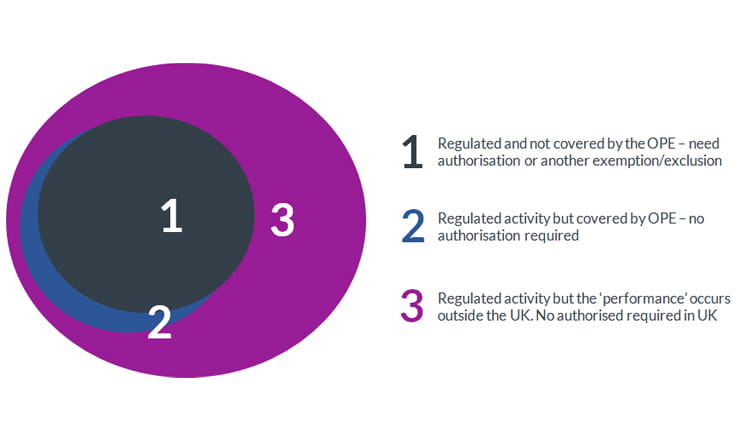

The general prohibition states that no person may carry on a regulated activity in the United Kingdom unless they authorised or exempt. Broadly – if you perform regulated activities like dealing, arranging, advising in respect to financial instruments like shares, bonds and derivatives in the United Kingdom (our emphasis) you need to be regulated.

A key part of this is that the activity needs to carried on "in the United Kingdom". As one of the major global centres for finance, a significant proportion of financial services are provided on a cross border basis. Where a non-UK firm provides a service to a UK person, the UK has historically taken a narrow view on whether that activity occurs in the UK.

Activities such as reception & transmission or portfolio management, as examples, are typically considered to be performed in the jurisdiction of the provider of the services, and not the UK wholesale client. Therefore there is no need for UK authorisation as the regulated activity is performed elsewhere (potentially requiring authorisation in that jurisdiction). This is sometimes referred to as the "characteristic performance" test.

In addition to the impact of the "characteristic performance" test, there is a specific "Overseas persons" exclusion ("OPE"). An “overseas person” is a person who carries on regulated activities but does not carry on any such activities, or offer to do so, from a permanent place of business in the United Kingdom. An overseas person is deemed not to carry on a regulated activity if they fall within the other requirements of the OPE. A condition frequently relied upon is that the transaction which is entered into was as a result of an unsolicited approach made by the UK investor to the overseas person As the activity is excluded under the OPE, no authorisation is required.

The combination of the OPE and the narrow characteristic performance test allows relatively frictionless services to be provided to UK wholesale firms from overseas entities in a number of areas such as broker dealers.

With both the OPE and the performance test there is no registration requirement, although typically firms take legal advice to understand where the boundaries lie.

The FCA's concern is that technological changes over the past few decades has meant that the OPE , which is largely unchanged since the 1980s, means that UK focussed businesses are being run using the exclusion. This is not the intention of the OPE.

The FCA therefore appears to want oversight of the uses of the OPE. Given that there is no requirement to notify the FCA at present, this is difficult for the FCA to do. Therefore we anticipate, at a minimum, a form of a registration or authorisation may be required. We also think it is likely that the FCA would be able to reject applications where it considers the firm unsuitable. This will create a quasi-regulatory regime at the very least and slow down services into the UK. At present, there are significant delays at the FCA dealing with core activities like new authorisations and change in control.

It is also possible that the activities where the OPE can be used will be narrowed. The FCA believes the nature and scale of activity that can be done in the UK without a permanent place of business here has increased and so trimming this back is on the agenda.

The FCA do not appear to focus expressly on the "characteristic performance" test but they do say "the overseas perimeter would benefit from greater clarity about when a regulated activity is being carried on in the UK". In our experience "clarity" from regulators often means providing guidance that is aligned with current market expectations. It is therefore feasible that activities that are not "performed" in the UK today will be performed in the UK in future, thus requiring either authorisation or reliance on (the modified) OPE.

Below we set out how this might work. Essentially, the regulatory perimeter in black will extend whilst the exclusions available will narrow.

The decision on the operation of the OPE is not the FCA's to make, as it would require changes to the Regulated Activities Order (although it can at the margins affect its operation through guidance).

There is another political angle to this that therefore needs to be considered. Chancellor Zahawi's recent Mansion House speech noted the Government's intention is to create a "… sector that is more open, competitive, green, and technologically enabled". It is hard to see how the speech from the Chancellor about liberalisation of the financial services regime meets with the FCA's aims to change a fundamental building block.

HM Treasury in its recent report indicated that "efforts to promote openness and clarity for international firms could build on reviewing the framework for overseas firms, including the well-regarded OPE, in ways consistent with maintaining market integrity and financial stability".

Having said that, since Brexit the OPE and characteristic performance test have allowed a number of EU firms to provide services into the UK that UK firms cannot provide into Europe. A financial service that can be provided from Libson or Ljubljana to London is considerably less likely to be able to be provided from London to Lisbon or Ljubljana without authorisation.

The implications of the proposals really do vary significantly for international firms and without final sight of proposed rules, it can be difficult but some implications may be:

This means firms would either need to be authorised and regulated in the UK, or transfer services to a UK regulated firm. In some cases, other exclusions and exclusions in the Regulated Activities Order may be available and certain agreements may be repapered. In some ways, it would be a rearrangement not dissimilar to that which firms worked through on Brexit. In the worst-case, withdrawal of services may be necessary.

We will watch Treasury and FCA proposals carefully. Firms may wish to consider whether to put in responses to the consultations.

The information provided is not intended to be a comprehensive review of all developments in the law and practice, or to cover all aspects of those referred to.

Readers should take legal advice before applying it to specific issues or transactions.