Low Carbon Pulse Edition 29

01 November 2021

Please click here for Edition 28 of Low Carbon Pulse, and click here for the Anniversary Edition of Low Carbon Pulse, which reflected on the 12 months since the publication of Edition 1 on October 6, 2020, and looking forward to the next 12 months. Click here and here for the sibling publications of Low Carbon Pulse, the Shift to Hydrogen (S2H2): Elemental Change series and here for the first feature in the Hydrogen for Industry (H24I) features.

After the weeks beginning September 20, 2021 (in New York), and September 27, 2021 (in Milan), the great and the good continued to prepare for the 26th session of the Conference of Parties (COP-26) of the United Nations Framework Convention on Climate Change opening this coming Sunday, October 31, in Glasgow, Scotland. The great and the good have been gathering in Glasgow for the last few days, and en route many of the great and good have been making announcements and caucusing.

As US Special Climate Change Envoy, Mr John Kerry, said in Milan: "The bottom line is, folks, as we stand here today, we believe we can make enormous progress in Glasgow, moving rapidly towards new goals that science is telling us we can achieve".

President of COP-26, Mr Alok Sharma, set out the UK Government Goals for COP-26, the fourth of those Goals including the finalisation of the Paris Rulebook. Mr Sharma has been quoted as saying that reaching agreement of the Paris Rulebook will be more difficult that achieving agreement of the Paris Agreement.

One senses that Mr Sharma is right, and yet just because something is difficult does not mean that it is not pursued. Third time lucky with the Paris Rulebook!

During this week-beginning October 25, 2021, five Low Carbon Pulse – COP-26 Countdown features were published covering the four key goals outlined for COP-26 by the UK Government as the host of COP-26 (the Four Pillars).

This Edition 29 of Low Carbon Pulse does not repeat the Four Pillars or the subject matter of them.

It is a little over 30 years since the United Nations Intergovernmental Panel on Climate Change (IPCC) released its First Assessment Report in 1990. In a little over 30 years, the mass of GHGs present in the climate system has doubled. Among other things, this increase in GHG emissions reflects increasing population, prosperity and urbanisation.

The bottom line is that by 2030, GHG emissions need to be reduced by 45% (at least) to ensure that average increases in global temperatures stay within the bottom end of the responsible range between the Stretch Goal and the Stabilisation Goal i.e., between 1.5OC to 2OC (Responsible Range), and a reduction of 50% is required to achieve the Stretch Goal. This analysis is drawn from the UNFCCC NDC Synthesis Report which synthesises information from the 164 latest nationally determined contributions (NDCs) communicated by the 191 Parties to the Paris Agreement as at July 30, 2021. While it is known that GHG emissions must be reduced, GHG emissions are projected to increase. It is the Synthesis Report that projects the Catastrophic Pathway.

In the week leading up to COP-26, the Commitment and Production Gap has probably received more concerned coverage in news feeds and opinion pieces than any other matter.

The United Nations Environment Programme (UNEP) publishes a production gap report annually. On October 20, 2021, the UNEP published the 2021 Production Gap Report (PGR) annually. Each production gap report assesses the gap between NDCs and the planned and projected fossil fuel production. The authors of the PGR note that as countries have made NZE commitments and increased their NDCs, they, "… have not explicitly recognised or planned for the rapid reduction in fossil fuel production that these targets will require".

The PGR notes that given current plans and projections, by 2030, the production of fossil fuels will exceed levels that are consistent with achieving the Stretch Goal; by 240% more in the case of coal, by 57% more in the case of oil and by 71% more in the case of natural gas. The "policy setting hand" and the practical, real world hand, are not coordinated. As a result, there is a gap.

If the gap is not bridged or narrowed, it is expected that the current bottom line (as projected) will result in at least a 16% increase in GHG emissions by 2030. This is not consistent with the Stretch Goal, rather it aligned with what United Nations Secretary General, Mr Antonio Guterres has termed a Catastrophic Pathway.

United Nations Secretary General, Mr Antonio Guterres, pulled no punches in his address to the United Nations General Assembly in September. Mr Guterres expressed extreme concern, critically, that the world is on a catastrophic pathway to a 2.7OC increase in average global temperatures compared to pre-industrial times (Catastrophic Pathway) without significant and immediate increases in the rate of GHG emission reductions. As is readily apparent from the science based reports: greater GHG emission reductions are needed, and the rate of those reductions needs to increase. No matter the direction from which discussion is approached, the discussion needs to coalesce around "greater and faster reductions".

The First Pillar (of the Four Pillars) for COP-26 contemplates staying within the Responsible Range, while "keeping in touch" with the Stretch Goal.

Earlier in 2021, Mr Thomas Bach, President of the Olympic Committee, suggested the addition of the word "Together" to the Olympic motto, Faster, Higher, Stronger. The rate of reduction in, and the rate of removal of, GHG emissions need to be faster and higher, and the commitments stronger.

More than this, Article 2.2 of the Paris Agreement provides: "This Agreement will be implemented to reflect equity and the principle of common but differentiated responsibilities and respective capabilities, in the light of different national circumstances".

Increased GHG reduction commitments (through increased NDCs) will bridge or narrow the gap in concept, but equally important as NDCs is the use of an accepted and common monitoring and reporting framework in compliance with which reductions in GHG emissions will be monitored, and, through that monitoring, measurement, and those determinations, GHG emission will be verified.

This will be achieved by the bolstering of the 2018 Paris Rulebook (developed but not finalised at COP-24 in Katowice, Poland, and COP-25 in Madrid, Spain) with the bolstered Rulebook being the Paris / Glasgow Rulebook. The 2018 Paris Rulebook was agreed in part in December 2018 at COP-24, and provides guidelines for countries to achieve the outcomes provided for under the Paris Agreement. Given that the 2018 Paris Rulebook was agreed in part, it is incomplete, critically around key elements of accounting and accountability for NDCs.

As has been noted by many commentators, because the Paris Agreement is a bottom-up agreement, Parties to the Paris Agreement set their own targets (i.e., their NDCs), set policies as the means of achieving those targets, set the standards used to account for them, and as such to monitor and to report on their achievement. Ideally, the Paris Rulebook will provided for standardisation.

For the author, while not headline grabbing, progress on the Paris Rulebook is the the most pressing outcome in achieving progress to NZE, along with increased NDCs and commitments to development and deployment of renewable electrical energy, critically, to monitor achievement to respond to circumstances in which progress is not being made, and to verify what progress has been made.

At the moment, the 2018 Paris Rulebook does not require countries to narrow or to bridge the gap between projected fossil fuel use and their NDCs. It is possible to see some folk seeking to "paper over the gap" by use of International Market Mechanisms under Article 6 of the Paris Agreement. Papering over a crack is not advisable. Papering over a gap, even less so.

One of the most debated areas, if not the most debated area, is the use of carbon credits (and cross-border emissions trading), including to bridge or to narrow the gap. This debate appears set to take centre stage.

The point of reference for the author continues to be the IPCC Sixth Assessment Report – Climate Change, The Physical Science Basis (2021 Report). It is understood that the 2021 Report is in the Final Government Distribution phase, a phase that is to end on November 26, 2021, being a date after COP-26 finishes.

During the weeks leading up to COP-26, a number of news outlets reported on "leaks" of correspondence arising from the consultation process as part of the Final Government Distribution phase. While the author has not seen any of the correspondence, given the nature of the Final Government Distribution phase, the author does not read too much into the reported correspondence: the science will not change; how to achieve NZE is the subject of debate, validly so.

By mid-February 2022, the Summary for Policymakers will be pretty much finalised. (The 2021 Report comprised a Summary of Policymakers in draft – see Edition 24 of Low Carbon Pulse.)

The 2021 Report continues to be the oracle, providing the range of outcomes from which COP-26 has to choose.

While frequent readers of Low Carbon Pulse will be familiar with the key provisions of the Paris Agreement, for convenience they are set out below:

| KEY PROVISIONS OF THE PARIS AGREEMENT FOR COP-26 |

|

|---|---|

|

Article 2.1: This Agreement … aims to strengthen the global response to the threat of climate change … including by: |

Article 4: In order to achieve the long-term temperature goal set in Article 2, Parties aim to reach global peaking of greenhouse gas emissions as soon as possible, … and to undertake rapid reductions thereafter in accordance with best available science, so as to achieve a balance between anthropogenic emissions by sources and removals to sinks in greenhouse gas in the second half of this century … . |

| Article 6: 1. Parties recognise that some Parties choose to pursue voluntary cooperation in the implementation of their nationally determined contributions to allow for higher ambition in their mitigation and adaptation actions and to promote sustainable development and environmental integrity. 2. Parties shall, where engaging on a voluntary basis … promote sustainable development, and ensure … integrity and transparency … and shall apply robust accounting … to ensure .. avoidance of double counting consistent with guidance adopted by the Conference of Parties … . |

|

As noted above, during this week beginning October 25, 2021, Low Carbon Pulse – published five COP-26 Countdown features dealing with the four key goals outlined for COP-26 by the UK Government as the host of COP-26 (the Four Pillars).

The Four Pillars are as follows:

It follows from the Four Pillars, and related matters the agenda items at or towards the top of folks' lists are likely to be:

NDCs and Paris Rulebook:

Commitments to NDCs, or commitments to increased NDCs, accompanied by the Paris Rulebook to provide a clear, monitorable and verifiable pathway towards NZE, are key to the success of COP-26. Progress on these matters will be a clear indication of the success of COP-26.

Commitments to, or commitments to increased NDCs, represent the first step for some countries, and longer strides for others. To avoid miscalculation of progress to achieving NDCs and NZE, the Paris Rulebook is needed, both to monitor (and to provide the basis for measurement and determination) and to verify reductions in GHG emissions, and to achieve efficient deployment of technologies and initiatives on a basis that recognises and responds to any non-achievement of GHG emission reduction commitments.

Also the Paris Rulebook is needed to provide a clear basis to monitor and to verify the use of carbon credits to offset compliance or mandatory obligations or to allow corporations to use carbon credits to manage their progress towards NZE.

Defined commitments to the development of: (i) Carbon Capture and Storage (CCS), and Carbon Capture Use and Storage (CCUS) including to allow the development of Blue Hydrogen production capacity are needed; and, (ii) renewable electrical energy capacity, solar and wind (off-shore and on-shore), to develop sufficient renewable electrical energy to allow the production of Green Hydrogen as soon as practicable, is needed. (See Editions 26 and 27 of Low Carbon Pulse, including under Government needed to guide to achieve timely development.)

The ever declining cost of photovoltaic solar electrical energy may be regarded as a function of markets working at their best, and critically, to lower the cost of producers of equipment, supplying domestic and international markets, allowing the deployment of photovoltaic solar at a scale that results in the lowest electrical energy costs in history, and the increasing development of battery electric storage systems (BESSs). Click here for a graphic entitled Electricity from Renewable Energy Sources is Now Cheaper than Ever.

In some markets, these outcomes have been achieved before use of photovoltaic solar has been incentivized.

As a result of these dynamics, the Levelized Cost of Energy (LCOE) for photovoltaic solar electrical energy has become the lowest of any source of electrical energy in many markets.

From COP-26, it is hoped that developing countries, including those in Africa, East Asia, South East Asia and the Pacific Islands, will emerge with funding support programs to maximise deployment of photovoltaic solar development, both roof-top and utility. Further, it is hoped that President Xi Jinping's proposal for a global high voltage direct current (HVDC) renewable energy network receives the "air-play" that it deserves.

It is clear that a number of countries and organisations attending COP-26 will seek to focus on carbon credits and trading in them, including to allow off-set against emission reduction commitments and liabilities, and the development of carbon credit trading. As noted above (and below), increased carbon credits, in theory, will narrow the gap between the projected increase in GHG emissions and the NDCs of some countries.

It is critical to keep in mind that the use of carbon credits, while important, will not achieve the level of GHG emission reductions required to achieve NZE. The effective use of carbon credits, and the development of trading platforms for high-quality carbon credits, will "buy time" for the corporations purchasing them and for the rest of us by slowing the rate of increase in GHG emissions.

The slowing of the rate of increase in GHG emissions will slow the rate at which we deplete the global carbon budget, but ultimately decarbonisation of activities giving rise to GHGs is required.

A number of commentators have suggested that a global price on carbon should be on the COP-26 agenda.

While a global price on carbon would link directly to the market for carbon credits, the author does not consider that a price on carbon is an appropriate agenda item for COP-26 or any Conference of Parties.

This is not because a price on carbon is not a good idea in the right setting, but because the imposition of a global price on carbon would have to take account of current policy settings (including current customs and excise duties and taxes on fossil fuels) in each country, and is "a third rail" that is best left untouched.

A carbon price is a tool used to encourage participants in markets to move to lower, low or no carbon technologies. In some countries a carbon price makes sense, but it makes sense only if it is set at a level that encourages the development and deployment of lower, low or no carbon technologies (and those technologies are available or on the horizon) – this is the logic for any carbon price, whether set through an emissions trading scheme or as a carbon tax, or both.

The "price on carbon versus technology" debate is one that the Federal Government of Australia has been sharing for a while: technology, not a carbon price (or in Australian parlance, a carbon tax), will result in progress to achieving NZE. The Federal Government of Australia is committing tax-payer money to support the development of technologies which the Government hopes will find a market.

The debate that the Federal Government of Australia shared is incomplete in that it ignores the rate at which reductions in GHG emissions need to be achieved, and that a price on carbon provides a benchmark for the cost of a lower, low or no carbon technology displacing carbon. This debate will no doubt continue.

On October 6, 2021, S&P Global Platts reported on the assessment of the US EIA (the US Energy Information Administration). The S&P Global Platts report notes that the projection of the US EIA in its International Energy Outlook (IEO) is that global energy demand will grow by 47% by 2050, and oil and natural gas will remain the largest source of energy.

The assessment of the US EIA "underscores the stark challenges ahead for transitioning away from fossil fuels and curbing global warming emissions".

The IEO is stark. It is the counterfactual to the aspirational NZE, and emphasises the importance of the reduction of GHG emissions by 45% (or more) by 2030, if not sooner. As noted in previous editions of Low Carbon Pulse, leaving decarbonisation to markets will not result in NZE.

As noted above, there is a Commitment and Production Gap. COP-26 will not resolve the Commitment and Production Gap, but this gap needs to be discussed, and the Paris Rulebook needs to address how Parties to the Paris Agreement will address this gap.

As noted above , and to provide emphasis, in the week leading up to COP-26, the Commitment and Production Gap has received more concerned coverage than any other matter.

Throughout 2021 the mass of and the speed at which publications have been released has increased, in part in anticipation of COP-26. This has been the case, in particular, since May 18, 2021.

Since May 18, 2021, in addition to the 2021 Report, the following reports have been published, earliest first, most recent last (all summarised in Low Carbon Pulse):

In the lead up to COP-26, many papers, reports and studies have been published. In the context of COP-26 the following seem the most relevant:

On October 5, 2021, the International Energy Agency (IEA) continued its prolific year with the publication of its Global Hydrogen Review 2021 (IEA GH2R).

As always with IEA publications, the IEA GH2R is both helpful and informative, and as such well-worth a read, and continues the consistent engagement of the IEA in respect of hydrogen (see The Future of Hydrogen Report). Of particular interest to the author is the Hydrogen Projects Database.

The key message from the IEA GH2R, in particular for the purposes of COP-26, is one that will be familiar to readers of Low Carbon Pulse: the role of Government is central to the development of both the Blue Hydrogen and Green Hydrogen industries, and as such the associated development of hydrogen-based fuels.

This key message is consistent with the messaging from the IEA since well before Edition 1 of Low Carbon Pulse. Edition 27 of Low Carbon Pulse (under A role for Government in the development of supply and demand for hydrogen) referenced an opinion piece from Wood Mackenzie: "… [COP-26] must go far far beyond setting new emission targets. Ensuring that hydrogen is not just a "fuel of the future", but a fuel that needs to be … implemented into global society from today [and] should be top of the agenda".

The IEA GH2R will be considered in detail in the October Report on Reports (in the Appendix to Edition 30 of Low Carbon Pulse).

On October 6, 2021, the US EIA published its International Energy Outlook (IEO). As noted above, the IEO may be regarded as an assessment of what supply and demand will be given current policy settings, and as such without material and significant initiatives that change this direction of travel. (The October Report on Reports will consider the IEO in detail.)

This IEO is a read for the positive realist, determined to press for progress on the basis of higher and faster GHG emissions, and stronger enforcement, together. This said, the positive realist needs to understand that the US IES may be regarded as plotting a demand / consumption curve above those plotted by others in the recent past.

On October 7, 2021, the IEA published its Curtailing Methane Emissions from Fossil Fuel Operations (CCH4R). It will be no surprise to readers of Low Carbon Pulse that the headline from the CCH4R is that the reduction in methane (CH4) emissions is "among the most impactful ways to combat near-term climate change".

As noted in the Anniversary Edition of Low Carbon Pulse, one of the areas of progress since October 2020 has been the recognition of the need to address CH4 emissions, culminating in the Global Methane Pledge, signed by the European Commission (EC) and the US on September 17, 2021. As at noon on October 29, 2021, 24 countries have committed since then, including Argentina, Indonesia, Italy, Mexico, and the UK, with New Zealand considering joining, and the Kingdom of Saudi Arabia has committed to joining.

The IEA has been advocating consistently for a focus on CH4 emissions for some time, and will no doubt continue to do so.

The CCH4R notes (as it has noted on a number of occasions), that: "Methane has contributed around 30% of the global rise in temperature to date … Emissions from fossil fuel operations present a major opportunity [to limit global warming in the near term] since the pathways to reduction are both clear and cost-effective".

The CCH4R will be covered in detail in the October Report on Reports (in the Appendix to Edition 30 of Low Carbon Pulse).

In passing, it is important to note that while the focus of the CCH4R is CH4 arising from the extraction, production and transportation of fossil fuels, CH4 arises from agriculture, forestry and other land use (AFOLU) and waste and waste water. At the same time as CH4 emissions from fossil fuel operations are being targeted, CH4 emissions from waste and waste water need to be addressed (see below A role for Government in decarbonising AFOLU and A role for Government in the development of Bioenergy).

As noted in other editions of Low Carbon Pulse, AFOLU is challenging, but addressing waste, in particular landfill, and waste water should be alongside addressing CH4 emissions from fossil fuel production. This requires policy settings and implementation from Government to align with the waste management system.

On October 13, 2021, the IEA published its World Energy Outlook 2021 (IEA WEO). The key message from the IEA WEO is that the world is in energy transition but the rate of progress towards energy transition, and the achievement of progress towards NZE, needs to increase.

The IEA WEO will be covered in detail in the October Report on Reports (in the Appendix to Edition 30 of Low Carbon Pulse).

On October 13, 2021, the International Renewable Energy Agency (IRENA) published its A Pathway to Decarbonize the Shipping Sector by 2050 (DESS Roadmap).

The DESS Roadmap notes that currently the shipping sector uses fossil fuels, and that it is necessary to displace fossil fuels so as to reduce CO2 emissions. The DESS Roadmap provides a description of the ways and means to the displacement of fossil fuels so as to achieve an 80% reduction in CO2 emissions by 2050.

Director General of IRENA, Mr Francesco La Camera provides a clear picture: "[The DESS Roadmap] clearly shows that cutting CO2 emissions in such a strategic, hard to abate sector, is technically feasible through [the use of] green hydrogen fuels."

IRENA contemplates that up to 70% of the fuels used in the shipping sector by 2050 will be hydrogen-based fuels. Without necessarily wanting to pick winners, IRENA suggests that the use of e-ammonia could provide close to 45% of the energy demand from the shipping sector by 2050.

In some ways, the DESS Roadmap may be regarded as conservative given the initiatives already "on the water", critically, the progress that the shipping industry is making in the use of hydrogen-based fuels (see Editions 26 and 27 of Low Carbon Pulse).

The shipping sector is increasing, some might say intensifying, efforts to reduce the GHG emissions arising from the sector. By way of a reminder, the shipping sector gives rise to up to 3% of global GHG emissions (expressed in CO2-e terms), with the International Maritime Organisation suggesting 2.9% and IRENA suggesting around the same. A recent article (entitled Enduring waves of climate change: Maritime Decarbonization, a tempest before the calm) from the ever accurate S&P Global Platts provides a balanced perspective, noting the scale of the task, balanced with the achievability of the task.

The October Report on Reports (contained in Appendix to Edition 30 of Low Carbon Pulse) will consider the DESS Roadmap in detail.

On October 19, 2021, the IEA published its paper Phasing Out Unabated Coal – Current status and three case studies (UAC Paper). The UAC Paper carries forward one of the key findings in the IEA WEO – critically, the need to end investment in new unabated coal-fired power plants, and to retrofit, and to repurpose, existing coal-fired capacity.

As is typical in IEA publications, the UAC Paper contains a number of recommendations: 1. Allow sufficient time for consultation and implementation of phase out plans; 2. Provide support for affected communities, including workers; 3. Ensure that security of electrical energy supply is maintained as "a cornerstone of phase-out policies"; 4. Implement carbon pricing; 5. Improve the climate for investment in clean electricity and the necessary infrastructure; and 6. Consider conversion of coal generation assets.

Recommendations 1 to 3, and 5 and 6 will come as no surprise.

The implementation of recommendation 4 (Implementing carbon pricing) may come as a surprise given the need to accelerate the retirement of coal-fired power generation is more about development of new renewable electrical energy capacity as soon as practicable, than use of a carbon price.

On October 20, 2021, the IEA published its report Achieving Net-Zero Electricity Sectors in G7 Members (NZE ES Report). The NZE ES Report was requested by the UK (which holds the G7 this year). As might be expected, the NZE ES Report builds on the finding from the IEA Roadmap published on May 18, 2021.

The NZE ES Report will be considered in detail in the October Report on Reports (in the Appendix to Edition 30 of Low Carbon Pulse).

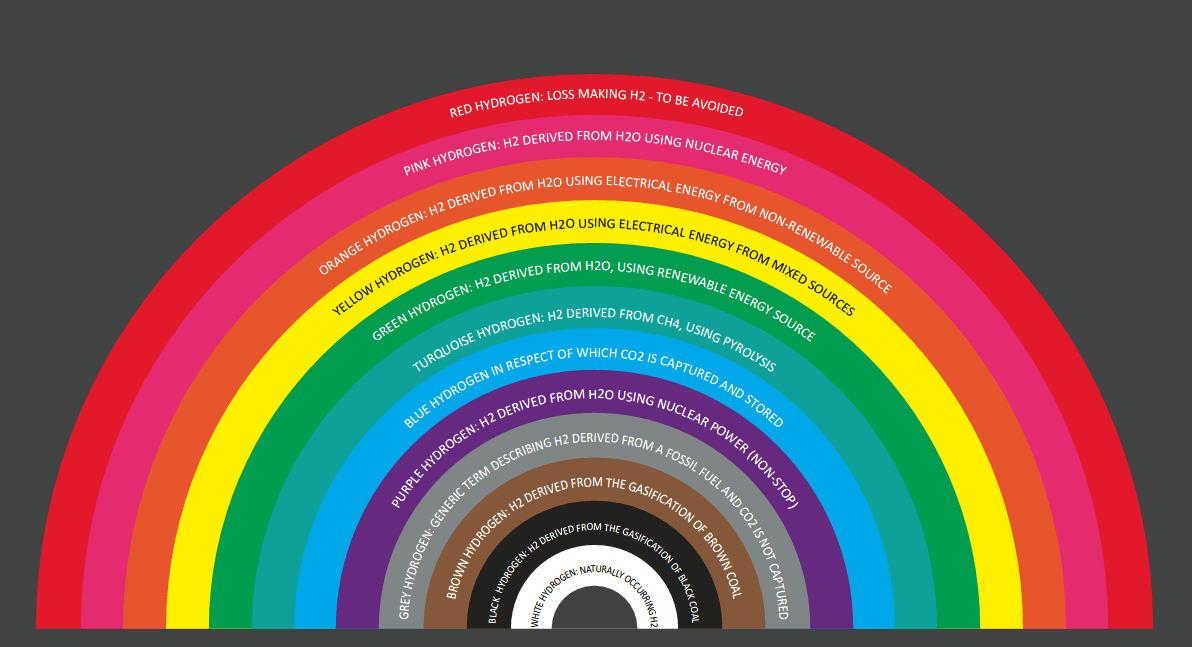

In the October 9, 2021 edition of The Economist, the venerable publication reflected on the size of the current hydrogen industry, at 90 million metric tonnes per annum (mmtpa) and USD 150 billion.

Given current technologies (steam methane removing, grey hydrogen production and gasification, black or brown hydrogen production), around 6% of the natural gas and 2% of coal production is used each year to produce this 90 mmtpa of hydrogen.

The production of the 90 mmtpa gives rise to between 850 and 900 mmtpa of GHG emissions, or around 1.8% of the 50 Giga-tonnes CO2-e GHG emissions arising each year.

As such, hydrogen produced using these technologies is not going decarbonise the production of energy carriers to displace hydrocarbons; rather CCS / CCUS to produce Blue Hydrogen and electrolysers and renewable electrical energy will do this.

The Economist notes the degree of difficulty and the scale of the endeavour. To remind the reader of the various colours of hydrogen, the Ashurst Hydrogen Rainbow is included below.

Ashurst Hydrogen Rainbow:

The Ashurst Hydrogen Rainbow (a creation of the author of Low Carbon Pulse), is intended to provide an aide memoire to the reader. It is noted that the author of Low Carbon Pulse took liberties with both the colour coding of hydrogen and the spectrum: adding Red Hydrogen (at the top of the Rainbow) to represent the difficulty of making a return on any early stage clean or low hydrogen project, and adding Grey, Brown, Black and White (at the bottom of the Rainbow) for completeness of the colours that are used to describe hydrogen.

On October 4, 2021, UK Prime Minister, Mr Boris Johnson announced that by 2035 all electrical energy dispatched to satisfy load in the UK would be matched by renewable electrical energy. This is the perfect response to the impact of the shortage of natural gas on the electrical energy prices in the UK: the best cure for higher prices is higher prices, resulting in increased supply or in a switch to another technology or increased use of an existing technology.

Stating the obvious, the switch to an existing technology is occurring, and needs to accelerate. Until the switch reaches a tipping point, the UK Government, like many countries around the world, needs an energy security policy (sufficient supply side to avoid sustained higher prices). While an inconvenient truth, the UK and EU countries may need more gas-fired power stations to provide required energy supply, and those gas-fired power stations will have to be developed with CCS / CCUS. As frequent readers of Low Carbon Pulse, and sister publications of Low Carbon Pulse, will know, this is a long-standing perspective of the author of Low Carbon Pulse.

On October 7, 2021, the United Arab Emirates (UAE) committed to reduce its GHG emissions to NZE by 2050 – see below (under GCC Countries update) for more detail.

Edition 28 of Low Carbon Pulse noted the good news arising from the United National General Assembly during the week beginning September 20, 2021, that Turkey had committed to ratify the Paris Agreement. The commitment had to be ratified by the parliament of Turkey. On October 8, 2021, the parliament of Turkey ratified the accession of Turkey to the Paris Agreement.

On October 18, 2021, the Republic of Korea (ROK) increased its NDC from 26.3% to 40% by 2030, compared to 2018. This is considered in more detail below under Republic of Korea (ROK) News.

On October 24, 2021, the Kingdom of Saudi Arabia (KAS) committed to reduce its GHG emissions to NZE by 2060. The commitment of the KAS, and the associated steps to implementation (see below under GCC Countries update) for more detail demonstrate in the clearest of terms the economic, environmental and social transformation that is upon us.

As note in Edition 28 of Low Carbon Pulse, the Federal Government of Australia has been the subject of scrutiny by the international community and its own citizens because it had not committed to the achievement of NZE by 2050.

On October 26, 2021, the Federal Government of Australia announced its commitments to NZE. (see below under Australia – Weighted Progress for the reported perspectives on the commitment)

The UK Government hosted the UK Global Investment Summit (GIS), on October 19, 2021.

Notable announcements from the GIS are captured in the following press release – click here – from the UK Government providing a high level overview of the outcomes and commitments from the GIS.

During the week of GIS, the UK Government announced two strategies – Net Zero Strategy:

Build Back Greener and Heat and Building Strategy. These strategies will be considered in detail in the October Report on Reports.

As foreshadowed in previous editions of Low Carbon Pulse, ahead of COP-26, current and relevant matters would be considered, including the roles to be played by key players.

Edition 28 of Low Carbon Pulse contemplated that Edition 29 would cover the Role of Government in decarbonising Agriculture Forestry and other Land Use (AFOLU) and the development of bio-energy. It contemplated also that the Role of Carbon Credits and Coal would be considered. We have covered Carbon Credits, but not Coal. (the LIAC Paper does this effectively)

Edition 28 of Low Carbon Pulse noted that AFOLU is hard to decarbonise. In many countries, some may say in most countries, agriculture has cultural, political and social significance. In the interests of food security and political expediency, in many countries agriculture receives direct and indirect funding support, including policy settings intended to ensure maintenance of the value of certain crops.

Given these dynamics, the decarbonisation of the AFOLU sector is best regarded, and is best calibrated, on a country by country, area by area, basis.

In this context, there is a role for Government in ensuring that it "does no harm" having regard to the areas within a country in which it seeks to set policies that will result in a reduction in GHG emissions. In the context of "doing no harm", there is a role for Government at a number of levels. In the collection of waste, rather than crop burning (over 3.5% of GHG emissions expressed in CO2-e terms), and providing value to landholders to avoid deforestation (close to 2.5% of GHG emissions). In these areas alone, there is close to 7% of the total mass of CO2-e GHG emissions "in play".

In addition, Governments can encourage afforestation and reforestation and wilding of land, and practices to reduce GHG emissions arising, including to provide value for these forms of land use, including by use of carbon credits. These activities have value in that they remove GHG emissions from the climate system. The removal of GHG emissions from the climate system means that the rate at which our global carbon budget is being depleted will slow. Governments are now acting on the ability of certain trees and crops to absorb CO2.

The most potent GHG emission arising from agriculture is CH4, including raising livestock (around 5.8% of GHG emissions expressed in CO2-e terms) and growing certain crops (up to 2.2%). (CH4 is more potent than CO2 (see Edition 27 of Low Carbon Pulse)).

As noted above, initiatives to collect waste, to change land use and to remove GHG emissions from the climate system will allow progress to decarbonising the AFOLU sector, but given the potency of CH4, more needs to be done. What needs to be done in terms of CO2 removal activities needs to be determined and planned by Governments. And countries that export products that have given rise to CH4 need to do more still.

A key part of planning needs to consider the trees, and other vegetation (green carbon), that can achieve the highest levels of CO2 absorption (sequestration capacity) on a sustainable basis within areas of countries. Governments are ideally placed to map and to monitor trees and other vegetation to assess the sequestration capacity of trees and vegetation, above and below ground.

In addition, the use of coastlines and the nearshore in certain regions of the world offer potentially vast sequestration capacity (blue carbon). For example, mangrove forests and swamps, and areas with sea-grasses and tidal marshes, provide ecosystems that can absorb CO2. For Government, the task is to assess how much of the coastlines and the nearshore can be used to progress the development of blue carbon sequestration capacity.

It is estimated that one mangrove tree will absorb 12.4 kg of CO2 a year on average. Taking the benchmark of the Kingdom of Saudi Arabia to plant 50 billion trees (see Edition 13 of Low Carbon Pulse), 50 billion mangrove trees will absorb 620 million metric tonnes (mmt) per annum (mmtpa). It is possible to plant 5,000 mangrove trees per hectare, with each hectare absorbing 62 metric tonnes (mt) per annum (mtpa) of CO2. 50 billion mangrove trees could be planted on 10,000,000 hectares.

In contrast, a palm tree will absorb around 2.3 kg of CO2 a year. On October 25, 2021, the US State of Florida announced plans to replace palm trees with native canopy trees, which absorb a greater mass of CO2. Palm oil trees are different, and the data on their ability to absorb CO2 has quite a spread. Taking the highest estimate of the spread at 57.6 mtpa per hectare, palm oil trees appear comparable with mangrove swamps. This is not to suggest deforestation and planting of palm oil trees (the broader challenges with palm oil are well known and beyond the scope of this Edition 29 of Low Carbon Pulse), rather it is to provide a point of comparison.

By way of further comparison, a pine free will absorb around 10 kg of CO2 a year. On the basis that there are approximately 1,000 trees per hectare, the pines trees in that hectare will absorb 10 mtpa of CO2.

"Higher, Faster, Stronger" is a good description for bamboo: bamboo is a super-absorber of CO2, storing CO2 in its biomass, particularly its root system (its extensive root system being good for soil quality, preventing soil erosion and assisting in the restoration of soil-depleted areas). For these reasons, the planting of bamboo may be regarded as integral to long-term agricultural redevelopment and agroforestry.

As with the reporting on the capacity of palm oil to absorb CO2, the reporting on the capacity of bamboo to absorb CO2 varies somewhat. At the higher end, one hectare of bamboo is reported to be able to absorb between 17 and 20 mtpa of CO2. Bamboo is fast growing, and mature groves of bamboo can be established within two to three years. Bamboo is an effective above ground carbon and below ground carbon absorber.

For every 10 million hectares of land used to grow bamboo, between 170 and 200 mmtpa of CO2 will be absorbed each year. India is estimated to have around 12.4 million hectares of bamboo groves.

For each country, an immediate focus should be the assessment and analysis of the use of trees, other vegetation and crops, best suited to the environment in which they are grown, including the return of land to the wild (and paying for the benefit of doing so). An assessment of this kind will yield an understanding of optimal land use, from both an economic and environmental perspective, and a means to realise value from carbon credits.

The IEA Roadmap and the IRENA WETO both identified the development of bio-energy capacity as key to achieving NZE under the scenarios outlined in them. As noted in previous editions of Low Carbon Pulse, bio-energy is energy derived or produced from biomass, whether that energy is in gaseous, liquid or solid form. Bio-energy is derived from organic matter, but not fossilised organic matter.

The sources of biomass for use as feedstock or fuel are many and varied, but in the context of GHG emissions, the organic waste stream arising from human activities provides a renewable resource that, if collected, processed and used, can reduce GHG emissions, avoiding or reducing CH4 (and CO2) on the decomposition of that organic matter, and the displacement of fossil fuels with that bio-energy.

The importance of the reduction in CH4 emissions in explained in Edition 27 of Low Carbon Pulse. Reflecting this, the EU and US have recently committed (in the Global Methane Pledge) to reduce CH4 emissions by a third within the next decade (see Edition 27 of Low Carbon Pulse).

For the production of bio-energy to be carbon-neutral, it must be combined with carbon capture and storage, BECCS, or with carbon capture and use or storage, BECCUS. For bio-energy production using BECCS to make a contribution to a reduction in GHG emissions, it must displace another electrical energy source or energy carrier source, and, in any event, it must result in a carbon neutral outcome (rather than a carbon removal outcome) so as not to give rise to an increase in GHG emissions.

This is where Government has a role to play. As has been noted in respect of CCS / CCUS in the context of carbon clusters (invariably located around ports and the hinterlands of ports), the storage of CO2 is likely to require Government funding support, and also Government risk support. It is no surprise that both the IEA Roadmap and the IRENA WETO contemplate tying the development of the bio-energy to CCS / CCUS to capture and to store the CO2 arising from the production of bio-energy.

Progress towards achievement of NZE is not a zero sum game. More than that, it is to be expected that there will be increased scrutiny of the life-cycle and GHG emission footprint of asset and infrastructure life, and responsibility for recovery and recycling of organic matter giving rise to GHG emissions (in the same way as with metals and mineral and plastics, which is a topic for another edition of Low Carbon Pulse).

Across all human activities, waste arises and GHG emissions arise. Globally, Government has a role to play in the development of waste management systems from the point of the waste arising to the point of recycling, re-use, or disposal, including in this context, the recycling and re-use of biomass, and the disposal into storage of CO2.

The broader AFOLU, waste and waste water sectors are estimated as giving rise to up to 95% of anthropogenic CH4 emissions globally. Given the impact of CH4 emissions on climate change, there is an immediate and present reason to capture the life-cycle of carbon in the broader AFOLU and waste and waste water cycles. Organic matter in waste and waste water decomposes. The rate of decomposition varies. On decomposition, CH4 and CO2 arise.

Capturing the life-cycle of carbon is best framed and achieved through Government collection and consolidation initiatives. These will include the derivation and production of biogas, and biomethane for pipeline gas, from waste to displace natural gas over time. Further, if CO2 arising on the production and use of biogas or any other biofuel is captured and used, and matched by new growth biomass to absorb an equivalent mass of CO2 arising on oxidation / use of that biogas or other biofuel, the promise of bio-energy will realised.

In the agricultural sector, the implementation of policy settings of this kind would become the core of an environmentally and economically sustainable sector, including by use of the digestate arising from the derivation and production of bio-gas, and the use of cover crops and perennial crops.

While this piece is intended to identify the role of the Government in the development of bio-energy, the author thought that it may be helpful to outline the role of Government more broadly in the waste sector as progression is made towards the achievement of NZE, and as such outline the policy settings that are emerging and likely will emerge.

As progress towards NZE is made, the mass of waste arising on the extraction of metals and minerals, on the manufacture of equipment and infrastructure, on the transportation and installation of that equipment and infrastructure, and at the end of the life-cycle of that equipment and infrastructure, will increase. The most prominent waste streams from progress towards the achievement of NZE are solar panels and wind-turbines, Net-Zero Waste if you will (not to be confused with the existing use of this phrase as to describe another policy setting – Net-Zero Waste to landfill).

More broadly, the policy settings for the management of E-Waste and Net-Zero Waste are very much in the process of being re-based in the context of E-Waste and formulated in the context of Net-Zero Waste. The phrase E-Waste is used to describe waste that arises from electronic equipment used for business, domestic, industrial or scientific use, including equipment needed for Information and Communications (ICE). In a recent report, it is estimated that between 2.1 and 3.9% of global GHG emissions arise from equipment that becomes E-Waste. In part, this reflects that the production of ICE gives rise to GHG emissions (including some of the more potent), housed in plastics that are not designed for recycling, using heavier metals, the life-cycle of which needs to be understood and captured. Ultimately, all residual materials needs to be captured for safe and sustainable recycling or disposal.

Improved and new policy settings are needed if extraction and manufacturing is to be decarbonised in the case of ICE, and if GHG emissions are to be avoided in the case of equipment and infrastructure manufactured and developed, for the purposes of achieving progress towards NZE.

Policy setting for recovery, recycling and disposal of materials arising at the end of life-cycle needs to be contemplated sooner rather than later, and the means of recovery, recycling and disposal developed by Government or with its support, and its use mandated.

Note:

Net-Zero Waste is not yet a concept, but for present purposes it includes waste that arises from the extraction, manufacture, transportation and use of equipment and infrastructure developed for the purposes of reducing GHG emissions, including on the extraction of metals and minerals used in the manufacture of solar panels and wind towers and turbines, and energy storage systems (including BESSs) on the manufacture of those panels, towers and turbines, and systems, and on recovery and recycling of resources from them at the end of their life-cycles, and the means of disposal of any material that cannot be recovered or recycled.

There has been considerable coverage around the role of carbon credits in achieving NZE, not least because of the record high prices being paid for carbon credits in both compliance / mandatory markets (Mandatory Markets) and in voluntary markets (Voluntary Markets).

In Mandatory Markets (typically, in the context of an emissions trading scheme structured as a-cap-and-trade), carbon credits have value if they can be used to acquit, i.e. can be used to offset, an obligation to match the GHG emissions arising from the activities of a corporation with emissions trading permits (ETPs) that organisation is required to acquire under that emissions trading scheme. In this context, the value of carbon credits will be a function of the operation of the Mandatory Market, including the market price of ETPs and the consequences (including liability) under that emissions trading scheme for not acquitting or being able to offset.

In Voluntary Markets, carbon credits have value to corporations that have committed to achieving GHG emission reductions (and in the longer term NZE on the basis of carbon neutrality). Previous editions of Low Carbon Pulse have covered the uses of words and phrases in this context, but ultimately, decarbonisation takes time, and needs to be achieved across Scopes 1, 2 and 3 emissions. To buy the time, while still reducing GHG emissions on a net-basis, corporations buy carbon credits. In this context, the value of carbon credits is less well-defined than in a Mandatory Market and will tend to depend on the position of the corporation buying the carbon credits, and whether the carbon credits are going to underpin a transaction (for example, the sale of carbon neutral cargo of liquified natural gas or oil or an investment).

Acknowledging that some folk will debate this, the perspective of the author is that ultimately decarbonisation of activities is the only means of achieving NZE, and as such the role of carbon credits is to place a value on activities that remove CO2 from the climate system: the value is quantified in mass, with one metric tonne of CO2 having a value. As NZE is achieved, the carbon sinks absorbing CO2 the subject of the carbon credits should be used to remove CO2 in the climate system on an absolute basis.

The benefit of the removal of CO2 from the climate system is that it reduces the rate at which the global carbon budget is depleted, and in the case of CO2 that is removed from the climate system that is not subject to a carbon credit scheme, that removal of CO2 gives rise to a net-reduction in the GHG emissions.

Generally the challenge with carbon credits is the monitoring, measurement and determination, and auditing and verifying (accounting and accountability) the mass of CO2 actually removed from the climate system and sequestered in a carbon sink.

As noted in Edition 16 of Low Carbon Pulse, it is thought that the mass of GHG emissions assumed to being sequestered in carbon sinks is greater than the actual CO2 that actually sequestered, and is being sequestered, in those sinks. This is important, because they need to be the same. If they are not the same, the purpose of carbon credits is not being achieved.

Specifically, the challenge with some carbon credits issued in some countries (developed and developing) is that carbon credits are issued in respect of activities that do not remove CO2 emissions from the climate system. Further, the basis of accounting and accountability in some countries does not provide a level of assurance that CO2 is being removed. For those purchasing carbon credits, this matters. The fact that there is an increasingly segmented market for carbon credits tends to reflect that this matters.

Carbon credits are issued by Governments, reflecting the policy settings of those Governments. It is hoped that at COP-26, there is discussion and progress as to the basis upon which carbon credits should be issued so as to provide a level of consistency globally.

Further, it is hoped that the basis of standards of accounting and accountability to be applied are developed, and that those standards are carried forward in the laws and regulations of each country issuing carbon credits, and compliance with those standards will be required so as to access the higher prices that are being paid for high-quality carbon credits.

The Visual Capitalist provides a Voluntary Markets 101 outline, among other things, outlining the four key participants in the voluntary carbon credit markets, project developers, standards bodies, brokers and end buyers. The link is accessed with a click. The link has an accompanying descriptive narrative. In passing, it is noted that Governments are key, both as framers and as possible participants in voluntary carbon credit markets.

In addition to the Visual Capitalist, Shell has recently published Exploring the Future of the Voluntary Carbon Market, developed by it in collaboration with BCG. The publication is well-worth a read, providing a balanced perspective. The October Report and Reports will consider the publication in more detail.

At this point in recent Editions of Low Carbon Pulse, sections have been included on Climate change reported and explained and Visualisation and Listening Platforms and Tools, and useful materials. To manage the length of this Edition 29 of Low Carbon Pulse, these sections are not included, but will return in future Editions.

On October 6, 2021, the United Arab Emirates (UAE) became the first Gulf Cooperation Council (GCC) country to commit to achieving NZE. This is a materially significant commitment in a global context, and for the UAE it will spark a once in a generation, or possibly even, as some have noted, a one-of-a-kind shift in the economy of the UAE, driven and effected by the level of investment required to effect the shift to what will be a photovoltaic solar and Blue Hydrogen and Green Hydrogen economy.

The UAE is ahead of the curve in many ways, having already realised capital through its program selling interests in infrastructure assets and selling down interests in operating businesses, including on listing of them.

In Arab News on October 9, 2021, Chief Executive of Engie in the Kingdom of Saudi Arabia (KAS), Mr Turki Al-Shehri, expressed considerable enthusiasm around the development of Green Hydrogen, contrasted with caution around the development of Blue Hydrogen projects because these projects have become "much more difficult" to finance.

While a number of commentators may have questioned the development of Green Hydrogen, those at the forefront of the development of Green Hydrogen projects are convinced of the need and that progress is occurring: " … it's a global energy changer. Green hydrogen is coming. Even before it was a buzzword, [Engie has been spending roughly] €60 million a year on green hydrogen research around the world".

The KAS has some of the best renewable electrical energy resources globally, and as a result, some of the world's lowest cost electrical energy: KAS has reliable sunshine rates during the day, and reliable winds at night. This was proved up further on October 18, 2021 as the KAS announced the Round 3 of the NREP (see KAS shortlists bidders on Round 3 of renewables below).

On October 10, 2021, Masdar (Abu Dhabi Future Energy Company) announced that it had signed a strategic agreement to explore renewable energy opportunities in the Republic of Turkmenistan. This builds on the commitment that Masdar has demonstrated regionally. As noted previously in Low Carbon Pulse, Masdar is a member of the elite club of global "go to investors" in the renewable energy sector.

Consistent with the role of Masdar as a member of the elite club of global "go to investors", Masdar has obtained a credit rating to assist in its facilitation of, and investment in, projects.

On October 14, 2021, it was announced that Fertiglobe (a joint venture between ADNOC and OCI Chemical (world leading producer of soda ash)) and Scatec (a leading renewable electrical energy producing corporation) have entered into an agreement with the Sovereign Wealth Fund of Egypt (SFE) to develop a 50 – 100 MW electrolyser to produce Green Hydrogen as feedstock for the production on Green Ammonia.

The Green Hydrogen production facility is to be located near Ain Sokhna, close to existing facilities of a subsidiary of Fertiglobe, EBIC. Under the agreement, Scatec is to build, operate and own (a majority interest) the Green Hydrogen facility, with the Green Hydrogen to be supplied to EBIC to produce Green Ammonia.

See: Scatec partners with Fertiglobe and the Sovereign Fund of Egypt to develop green hydrogen as feedstock for ammonia production in Egypt; Fertiglobe Partners with Scatec and the Sovereign Fund of Egypt to Develop Green Ammonia Project in Egypt

On October 11, 2021, the Saline Water Conversion Corporation and Cummins announced that they intend to develop a hydrogen production facility in the KAS.

See: Cummins website; Saline Water Conversion Corporation website

On October 16, 2021, Huawei Digital Power (HDP) and SEPCOIII (EPC contractor for the Red Sea Project as part of the development of NEOM (see Update on NEOM below)) signed a contract under which HDP is to supply a 400 MW / 1,300 MWh BESS.

See: Huawei to Power the World's Largest Energy Storage Project

On October 17, 2021, it was reported widely that OQ (the Omani state-owned energy company) had signed a Joint Development Agreement with Dutco, Linde and Marubeni to undertake feasibility studies to assess the development of a 400 MW Green Hydrogen and Green Ammonia production facility (SalalahH2 Project) within the Salalah Free Zone in Oman. The SalalahH2 Project will make use of OQ's existing ammonia production plant at Salalah.

As reported in previous editions of Low Carbon Pulse (see Editions 18, 20 and 26), OQ is progressing a Green Hydrogen within the Duqm Special Economic Zone with DEME (leading Belgian corporation).

Edition 14 of Low Carbon Pulse reported on the Round 2 of the National Renewable Energy Program (NREP). At the inauguration for the Sakaka IPP on April 8, 2021, Crown Prince Mohammad bin Salman bin Abdulaziz announced the results of the tenders for seven large-scale solar capacity projects under. The seven new projects are to be located in Jeddah, Madinah, Quarayyat, Rafha, Rebigh, Al Shuaiba and Sudair.

The 600 MW Al Shuaiba photovoltaic solar project was being awarded on the basis of a world record low bid price for electrical energy of USD 0.0104 kWh (a little over 1 cent per kWh, or USD 10.40 per MWh). The Sudair photovoltaic solar project was awarded with the second lowest bid price of USD 0.01239 (1.239 cents per KWh or USD 12.39 MWh). On development, the Sudair photovoltaic solar project will be the Kingdom's largest solar project, comprising around 1.5 GW of installed capacity. Approximately 3.6 GW of energy was contracted under Rounds 1 and 2 of the NREP.

On October 18, 2021, it was reported widely that KAS' Renewable Energy Project Development Office (Repdo) had shortlisted bidders for Round 3 of the NREP, with 1.2 GW to be contracted under Round 3. There two categories of project in Round 3, Category A and Category B.

Category A projects are the 120 MW Wadi al-Dawasir PV IPP (WADIPP) and the 80 MW Layla PV IPP (LIPP). It is understood that TotalEnergies and Tamasuk Holding Company and the Acwa Power Consortium (comprising Acwa Power, SPIC (Huamghe Hydropower Development Company) and WEHC (Water and Electric Holding Company) ranked first and second on the WADIPP and Acwa Power Consortium and Alfanar ranked first and second on the LIPP.

Category B projects are the 700 MW Al-Rass PV IPP (ARIPP) and the 300 MW Saad PV IPP (SIPP). It is understood that the Acwa Power Consortium and Jinko Power ranked first and second on the ARIPP and that Jinko and Masdar ranked first and second on the SIPP.

As noted above, the Round 2 of the NREP resulted in a world record low bid price. Round 3 of the NREP has not quite resulted in the same outcome, but the pricing is nevertheless at a level that continues the narrative about low photovoltaic solar costs. It is reported that the levelized cost of electricity (LCOE) bids have tariffs at the following: WADIPP US cents 1.9 kWh, LIPP US cents 3 kWh, ARIPP US cents 1.5 kWh and SIPP US cents 1.5 kWh.

On October 19, 2021, on the sidelines of the UK Global Investment Summit (see section entitled G20 activity and commitments in the lead up to COP-26 above), Qatar Energy (formerly Qatar Petroleum, the state owned leading international energy corporation) and Shell (leading global international energy corporation) signed an agreement under which they will pursue jointly a Blue Hydrogen and Green Hydrogen project in the UK in which they can invest jointly.

On October 24, 2021, Crown Prince Bin Salman announced that the KAS would reduce its GHG emissions to NZE by 2060, with a reduction of 278 million metric tonnes per annum (mmpta) of GHG emissions by 2030. The financial capacity of the KAS makes the achievement of NZE by 2060 a high probability.

For these purposes, the Crown Prince announced that the KAS would invest USD 186 billion, join the Global Methane Pledge (see Edition 27 of Low Carbon Pulse), plant 450 million trees by 2030 and rehabilitate 8 million hectares of land. It is estimated that the planting of trees and the rehabilitation of land will reduce the CO2 emissions by 200 mmtpa. This initiative of itself will make a meaningful contribution to progress towards NZE.

On October 24, 2021, the world's largest corporation, Saudi Aramco, announced that it would target the reduction in GHG emissions to NZE by 2050.

On October 27, 2021, Saudi Aramco announced that it had signed a memorandum of understanding with InterContinental Energy and Modern Industrial Investment Holding Group to develop Green Hydrogen and Green Ammonia production facilities in Saudi Arabia. As readers of Low Carbon Pulse will be aware, InterContinental Energy is involved in large scale renewable electrical energy and Green Hydrogen and Green Ammonia projects in Australia and in the UAE.

On October 27, 2021, Abu Dhabi National Oil Company (ADNOC) and Emirates Water & Electric Company (EWEC) formed a clean energy partnership under which ADNOC is to be supplied by EWEC with clean energy matching 100% of ADNOC's electrical energy load.

EWEC will supply clean energy from nuclear and photovoltaic solar sources to ADNOC under an off-take agreement. This establishment of the partnership, underpinned by the off-take agreement, is aligned to achieving NZE by 2050.

The development of NEOM, the smart city, in Tabuk Province, on the coast bordering the Red Sea is progressing, and it is understood that visitors (including tourists) will be welcome from 2024. Key to the development of NEOM is that it is to be powered by 100% renewable electrical energy, including the use of Green Hydrogen. On October 30, 2021, fuelcellsworks.com provided a helpful update.

Recent editions of Low Carbon Pulse have outlined the policy settings and the private and public sector investment initiatives in India. On October 7, 2021, pv magazine, reported on a study from Lappeenranta-Lahti University (often mentioned in Low Carbon Pulse) and Wärtsilä.

The headline from the study is that using an all renewable electrical energy system (with 76% photovoltaic solar), and appropriate levels and location of BESS, the cost of electrical energy in India could be reduced by up to 50% by 2050, while at the same time making a major contribution to progress towards NZE.

The study (and other publications) tend to feed confidence that in respect of the development, the renewable electrical energy progress is likely to be made to achieve NZE across the electrical energy sector. This should not be taken for granted, but it is possible for the optimist to conclude that we will get there. The electrical energy sector is however the easiest part of the global economy to decarbonise. The difficult to decarbonise sectors (including cement, chemical and petrochemical, glass and iron and steel) and the transport sector (aviation, road freight and shipping) remain.

On October 28, 2021, pv-magazine, noted that India is expected to install 14 GW of photovoltaic solar capacity in calendar year 2021, having installed 8.8 GW of capacity in the first nine months. As noted in previous editions of Low Carbon Pulse, the development and deployment of roof-top photovoltaic solar in India is highly prospective. It would appear that this assessment is being realised with 2 GW of the 8.8 GW installed in the first nine months of 2021 being roof-top photovoltaic solar.

On October 29, 2021, pv-magazine, noted that scientists at the KPR Institute of Engineering and Technology have developed a process to recycle silicon from solar panels at the end of their life-cycle. If the process is scalable, it seems to the author to be a significant shift in process technology.

On October 29, 2021, pv-magazine reported that tenders have been invited for the development of "advanced-chemistry battery cell manufacturing units in India". The tender is open to applications until December 31, 2021. It is reported that bidders must commit to setting up a minimum of 5 GWh of capacity to qualify for subsidies.

Edition 19 of Low Carbon Pulse reported that on June 1, 2021, India and the UK had enhanced their existing partnership to provide for cooperation in sharing thinking around policy settings, which in turn will respond to, and drive, technology development and investment as both countries progress to electrified and hydrogen economies, driven by the development of renewable electrical energy. More broadly, and in the context of specific outcomes, the provision and sourcing of sustainable finance will be a key part of electrification and the development of a hydrogen economy, in particular clean energy and clean transport technologies and solutions, and the shift to green and to greened businesses.

On October 11, 2021, h2-view.com, reported that India and the UK intend to build on, or rather refine further, their collaboration, through a Government-to-Government agreement so as to contribute to the acceleration of progress towards the development clean energy capacity. The Government-to-Government agreement was formalised at a meeting of India's Minister for Power and New & Renewable Energy, Mr Raj Kumar Singh, and UK Energy Secretary, Mr Kwasi Kwarteng on October 8, 2021. It is understood that in the context of COP-26, the ministers discussed the launch of the India and UK Government Global Green Grid – One Sun One World One Grid Initiative.

The Government-to-Government agreement with the UK follows the announcement from the meeting of the Quad countries (US, India, Japan and Australia) in late September as which it was agreed: 1. to cooperate to allow the development of a green-shipping network, with each country to work with each other country to reduce GHG emissions arising from the shipping value chain; 2. to establish a Clean Hydrogen Partnership, including for the purposes of technology development and scaling up of hydrogen production on an efficient basis, with the intention to stimulate demand to accelerate trade in clean hydrogen in the Indo-Pacific region; and 3. to increase the Indo-Pacific region's resilience to climate change by improving climate change information sharing and disaster-resilient infrastructure.

Edition 3 of Low Carbon Pulse reported on the commitment of ROK to achieving NZE by 2050. Since the commitment to NZE made on October 28, 2020, there has been expectation that ROK would increase its NDC from 26.3% by 2030 compared to 2018.

On October 18, 2021, the ROK increased its NDC to 40% by 2030 compared to 2018. As with the increased NDC to which Japan committed in April 2021, this may be regarded as a challenging target for ROK. Nevertheless, it is a target that ROK will able to achieve.

On October 22, 2021, DFC agreed with Korea West Power and KEPCO to develop a Pure Biogas (Hydrogen) fuel cell R&D project.

On October 25, 2021, it was announced that Bloom Energy and SK are to expand their blooming partnership to fortify their market leadership in the use of fuel cell technology to generate electrical energy and to establish leadership in the hydrogen economy. The budding and then growing nature of the relationship between Bloom Energy and SK has been covered in Low Carbon Pulse (see Editions 4, 17 and 22).

Leaving the poor puns to one side, the expansion of the partnership is good for each corporation and more broadly – both organisations are at the forefront of early adoption of fuel cell technology and first movers in the development and deployment of it. The arrangements underpinning the expansion include SK contracting for equipment supply and service provision (estimated at USD 4.5 billion), and a further equity investment by SK in Bloom Energy.

See: Bloom Energy's announcement

On October 26, 2021, it was reported widely that Korean Southern Power (KOSPO) had opened the new Incheon Bitdream Fuel Cell Power Plant (Bitdream FCPP). The Bitdream FCPP uses fuel cell technology supplied by POSCO Energy and Doosan Fuel Cell. The Bitdream FCPP is reported to have capacity of 78.96 kWh, which can be used to supply electrical energy to up to 250,000 households and hot water for up to 40,000 households. The Bitdream FCPP is reported to have capacity of 78.96 kWh, which output can be used to supply electrical energy to up to 250,000 households and hot water for up to 40,000 households.

The opening of Bitdream FCPP is further realisation of the use of the power companies to use fuel cell technology (see Edition 2 of Low Carbon Pulse).

Edition 28 of Low Carbon Pulse included a piece entitled, Australia – A Curate's Egg. This description appears unlikely to be revised any time soon.

On October 13, 2021, the IMF released its Word Economic Outlook. In addition to the role of Australia as a key producer of iron ore, the IMF noted the importance of the cobalt, nickel and lithium resources of Australia for the purposes of the required expansion of resources to supply the global battery industry.

The IMF notes that demand for the supply of these key metals will increase dramatically as the scale of the renewable electrical energy industry increases, and an associated increase for battery storage arises, principally for battery electric vehicles (BEVs) and battery electric storage systems (BESSs).

By way of background or as a reminder, the five key metals in the "battery age" (at least for the time being) are aluminium, copper, cobalt, nickel and lithium. It is anticipated that demand for: 1. aluminium will increase to allow "light-weighting" to occur, particularly across the transport sector; 2. copper will increase, with demand for BEVs and grids and infrastructure (distribution and transmission) and machinery generally; 3 cobalt is less certain, with its demand profile dependent on technology development; 4. nickel will increase, with increased supply of nickel effectively responding to the new demand, and in the context of increased demand for (and therefore use of) nickel, stainless steel production will be the primary driver; and 5. lithium will increase to satisfy demand for lithium-ion batteries, in particular in the stationary energy sector, critically for BESSs.

As noted in Edition 22 of Low Carbon Pulse (in a feature on Form Energy), iron (using iron-air technology) could soon be joining these five metals as key metals in the "battery age". If this potential is realised, Australia will continue its role, and even enhance its role, as a key source of metals and minerals as raw materials to support progress towards the achievement of NZE.

In Edition 28 of Low Carbon Pulse, it was reported that the Federal Government of Australia had yet to commit to meaningful GHG emission targets or to NZE by 2050. As a result, for some time, the Federal Government of Australia has been under scrutiny by the international community and its own citizens: at once both the lucky country and the recalcitrant country, a country that could lead but a country that chooses not to do so.

On October 26, 2021, the Federal Government of Australia committed to achieving NZE by 2050. This commitment was not accompanied by meaningful GHG emissions targets on route to NZE. The approach manifest in the commitment to NZE by 2050 is consistent with the technology versus carbon tax debate that the Federal Government of Australia has been sharing in support of the approach that it has been taking (see section above entitled A price on carbon).

The commitment to NZE has been criticised from all sides. For those in favour of the commitment to NZE, the means of achieving NZE has been described as more "prayer than policy" due a lack of meaningful commitments to GHG emission reductions before 2030, and an absence of a staged pathway to achieving NZE by 2050. For those not in favour the commitment to NZE, the criticism is best described as variable, and none of it capable of withstanding reasoned scrutiny.

On October 13, 2021, Premier Annastacia Palaszczuk committed her State of Queensland to progressing to NZE by 2050. This commitment followed a vote the Queensland Parliament on October 12, 2021. This commitment came in a week packed full of announcements about the development of the Green Hydrogen industry across Queensland.

During the week beginning October 25, 2021, the State of South Australia, continued its progress towards becoming a 100% renewable electrical energy State. The State Government of South Australia is committed to achieving net 100% renewables by 2030. The events of the last week tend to indicate that the State of South Australia will achieve this target as early as 2025 at the current rate of progress.

On October 25, 2021, ElectraNet announced the installation of four synchronous condensers (in effect acting as spinning reserve). The installation of the synchronous condensers means that the restrictions on the dispatch of renewable electrical energy across the ElectraNet grid are not as stringent as previously under certain conditions: the restrictions providing a limit to the dispatch of variable renewable electrical energy sources to the grid so as to be assured of continued integrity and stability.

As reported in previous editions of Low Carbon Pulse, the State of South Australia has been a stellar performer, but during the last week it has eclipsed previous achievements with photovoltaic solar and wind reaching 81% at the start of the week, and 85% over three days of the last part of the week.

On October 29, 2021, the State of Victoria reported that it achieved a 25% reduction in GHG emissions compared to 2005, between 2005 and 2019. The State Government of Victoria has delivered on its pledge to reduce GHG emissions by 20% by 2020 (in fact it is has exceeded it), and is well on the way to delivering on its pledges to reduce GHG emissions by between 28% to 33% by 2025, and to between 45% to 50% by 2030.

As has been noted previously in Low Carbon Pulse, the eight States and Territories of Australia are both ambitious and progressive in reducing GHG emissions and progress towards achieving NZE. The ambition and that progressiveness are not static.

Edition 28 reported on the publication by the Australian Hydrogen Council of its Unlocking Australia's hydrogen opportunity. On October 29, 2021, a Wood Mackenzie publication outlined further the scale of the opportunity for Australia.

Previous editions of Low Carbon Pulse have covered the policy settings for energy transition in PRC. On October 10, 2021, the visualcapitalist.com, published five graphics that allow the viewer to visualise the transition from now to 2060 (the year by which the PRC has committed to achieve NZE).

On October 12, 2021, President Xi Jinping made a speech to the fifteenth conference of the parties to the Convention of Biological Diversity. President Xi confirmed the commitment of the PRC to achieve peaking of GHG emissions by 2030, and NZE by 2060. (Edition 30 of Low Carbon Pulse will include a one page summary of the outcomes from COP-15 to the Convention of Biological Diversity.)

To deliver on these commitments, President Xi said that it would be necessary to introduce policy settings (named "l+n") to achieve peaking of GHG emissions and then NZE. For these purposes, President Xi noted the need to increase the installation of photovoltaic solar and wind in desert areas of the PRC.

This is not new (having been noted in Edition 21 of Low Carbon Pulse, and confirmed in the next piece), but it may be regarded as further demonstration of the commitment of the PRC to mobilise sufficient renewable energy resources to achieve peaking and NZE, and consistent with the prospect of use of High Voltage Direct Current (HVDC) cables to deliver renewable electrical energy.

On October 29, 2021, it was reported widely that the PRC's National Development and Reform Commission (NDRC) confirmed that the development of a number of renewable electrical energy projects was proceeding across a number of provinces in the north and north-west of the PRC – Gansu (12.85 GW), Inner Mongolia (2 GW of photovoltaic solar), Ningxia, Qinghai (10.9 GW), Shaanxi (2 GW), and Xinjiang (GW). Once completed, the projects will have combined installed capacity in the region of 30 GW. It is understood that ultra-high voltage connection will be used for the purposes of transmission from generation to load, with some projects to deploy hydrogen energy storage systems (HESS).

As noted in previous editions of Low Carbon Pulse (and touched on above, under A role for Government in the development of Bioenergy), bio-energy is energy derived or produced from biomass, whether that energy is in gaseous, liquid or solid form. Bio-energy is derived from organic matter, but not fossilised organic matter.

Note: For the production of bio-energy to be carbon-neutral, it must be combined with BECCS or BECCUS. For BECCS / BECCUS to make a contribution to a reduction in GHG emissions, it must displace another electrical energy source or energy carrier source, and, in any event, it must result in a carbon neutral outcome (rather than a carbon removal outcome) so as not to give rise to an increase in GHG emissions.

On October 5, 2021, a report entitled CCUS Development Pathway for the EfW Sector, produced by Eunomia Research & Consulting, commissioned by waste company, Viridor, notes the ability of the EfW sector to help underpin the continued development of the CCS / CCUS sector in the UK, effectively BECCS and BECCUS.

On October 7, 2021, rechargenews.com, Repsol (world leading oil and gas corporation, head-quartered in Spain) announced plans to develop 200 MW of biogas / biomethane steam reforming capacity (to derive hydrogen from biomass itself derived from biomass) to produce Blue Hydrogen, and 350 MW of electrolyser capacity, powered by renewable electrical energy from 1.8 GW of photovoltaic solar and wind, to produce Green Hydrogen. It is anticipates that this clean hydrogen capacity will be developed by 2025, with around USD 1.5 billion earmarked for these initiatives alone.

On October 18, 2021, the-eic.com, reported that this was part of broader initiatives involving the development of 20 GW of renewable electrical energy by 2030, and an investment of €2.5 billion to develop a hydrogen chain by 2030, as part of its renewable hydrogen strategy, with 550 MW to be developed and deployed by 2025 (200 MW of Blue Hydrogen and 350 of Green Hydrogen capacity, as noted above).

See: Repsol will invest €2.549 billion to boost renewable hydrogen

On October 17, 2021, biofueldigest.com, reported that Haldor Topsoe (leading technology provider, including electrolysers and its eSMR technology) has commenced operation of a demonstration plant that derives methanol from biogas (a combination of CO2 and CH4 for the most part, derived from biomass). It is stated that the plant produces sustainable methanol, and has the capacity to produce 10,000 litres of CO2 neutral methanol.

On October 29, 2021, it was reported widely, that a site had been secured by CHBC (a member of Yosemite Clean Energy) to develop a carbon-negative renewable hydrogen and renewable natural gas (RNG) production facilities in Oroville, California. As reported, 31,000 kgs (31 metric tonnes) a day of RNG and 12,200 kgs (12 metric tonnes) a day of renewable hydrogen will be produced.

A rechargenews.com article notes that: "Because biomethane is produced from plant matter that absorbed CO2 from the air as it grew, the gas which is produced in large tanks known as anaerobic digesters – it is said to be carbon neutral when burned or cracked". As readers of Low Carbon Pulse will know, this is not incorrect, but it is important to add that CO2 and CH4 arises from the production of biogas / biomethane, and from the production of hydrogen from it, and that CO2 and CH4 needs to be captured. Of course, the hydrogen gives rise to no GHG emissions at the point of use other than water vapour which, while is a GHG emission, does not remain in the atmosphere in the same way that CO2 and CH4 (and other GHGs) do.