Low Carbon Pulse Edition 25

27 August 2021

Please click here for Edition 23 of Low Carbon Pulse. Please also click here and here for the first two articles in the Shift to Hydrogen Series (S2H2): Elemental Change series: the S2H2 series provides a narrative and perspective on hydrogen generally. Please click here for the first feature in the Hydrogen for Industry (H24I): the H24I features provide an industry by industry narrative and perspective.

The third article in the S2H2 series will be published within the next few weeks: the delay in publication of the UK Hydrogen Strategy (UKH2S) in July resulted in a change of plan, but the publication of the UKH2S means reversion to the original plan to publish an article on Hydrogen Plans, Roadmaps, and Strategies. An article on CCS / CCUS will follow in October.

A PDF version of this article is available for download below.

The Intergovernmental Panel on Climate Change (IPCC) report, Climate Change 2021, The Physical Science Basis (2021 Report) was published on August 9, 2021, and reported on in Edition 24 of Low Carbon Pulse.

Readers of Low Carbon Pulse will be aware that since May 18, 2021 the following reports have been published, earliest first, most recent last (all summarised in Low Carbon Pulse):

While each report is different, taken together, these reports provide consistent messages and themes, foremost among them is the need for acceleration towards net-zero greenhouse gas emissions (NZE) at a greater rate (to many at a considerably greater rate) than is currently contemplated. Acceleration requires increased nationally determined contributions (NDCs) under the Paris Agreement, in particular among the countries that are progressed further than others in achieving NZE, and the need for decarbonisation of activities, rather than the use of carbon credits / permits (CCPs), with the use of CCPs to accelerate negative greenhouse gas emission reduction initiatives (NGHGRIs).

As noted in Edition 24 of Low Carbon Pulse, the causes of, and the cures for, climate change are known, critically, what is needed to slow, and to peak greenhouse gas (GHG) emissions and then to accelerate the reduction of GHG emissions and to remove them to as to achieve the Stabilisation Goal (if indeed the Stretch Goal is not achievable).

As noted previously in Low Carbon Pulse, two of the three objectives in Article 2 of the Paris Agreement (all three are set out below) have tended to be forgotten (some may say neglected), at least in policy setting:

"Holding the increase in the global average temperature to well below 2OC above [Stabilisation Goal] pre-industrial levels and pursuing efforts to limit the temperature increase to 1.5OC above [Stretch Goal] pre-industrial levels, recognizing that this would [reduce significantly] the risks and impacts of climate change;

Increasing the ability to adapt to the adverse impacts of climate change and foster climate resilience and low greenhouse gas emissions development, in a manner that does not threaten food production; and

Making finance flows consistent with a pathway towards low greenhouse gas emissions and climate-resilient development".

The thinking behind these objectives is sound, with data continuing to underline that action is needed consistent with the sound thinking. It is worth recounting that all policy settings, and private sector initiatives, related to NZE, can be tied back to the three objectives in Article 2 of the Paris Agreement. Those framing the Paris Agreement were aware that climate change was "along-side us", that it would have an adverse impact on us, resulting in the need to adapt to its adverse impacts, at the same time as decarbonising activities giving rise to anthropogenic GHG emissions.

Given the extreme climate change induced events during the 2021 Northern Hemisphere summer, including droughts, floods, extreme heat waves, and forest fires (and rain falling on the summit of the Greenland Ice Sheet for the first time on record), it is to be expected that there will be a greater action on adapting to climate change, and its threat to food production.

In Europe, with the settlement of the locations of many communities pre-dating the pre-industrial era, it has become apparent that certain locations are no longer suitable for activities undertaken at them: borrowing the language of the moment, there will be a need "to build back better" and differently. This has brought home to many the existential challenges for those with island homes.

As a straight-talking Texan known to the author said in early June 2021: "When it rains, it rains too much, when it's hot, it's really hot, too hot. Y'all can deny the reason for it, but not the fact of it".

There is a tool developed by the US National Aeronautics and Space Administration (NASA) that makes it possible to visualise the possible levels of flooding that certain areas of the world may experience at different times based in increased sea-levels (and modelled variables).

One of the maps that has been shared is one showing areas of London that may be subject to frequent flooding by 2030 if extreme weather events occur. For those who live or work in London, or who have done so, the Extreme Weather Flood Map brings home the adverse impacts of climate change.

While the 2021 Report focuses on GHGs, carbon dioxide (CO2), methane (CH4) and nitrous oxide (N2O), they are not the only GHGs.

On August 18, 2021, nature.com reported on elevated levels of tetrafluoromethane (CF4) and hexafluoroethane (C2F6) emissions in the climate system. The report notes that the likely sources of the elevated levels of CF4 and C2F6 are the PRC (aluminium smelters) and Japan and South Korea (semi-conductor factories).

During the two week cycle of this edition of Low Carbon Pulse, another graphic from the Visual Capitalist (see Editions 23, 21 and 20 for other graphics from the Visual Capitalist) has come to the attention of the author. This time the graphic is in the form of a globe indicating the spread of countries from which GHG emissions arise.

Edition 23 of Low Carbon Pulse reported that the US infrastructure investment package (IIP) was nearly done. On August 10, 2021, the IIP "got done": by a vote of 69 to 30, the US Senate passed the Infrastructure Investment and Jobs Act (IIAJA).

From the US Senate, the IIAJA has made its way to the House of Representatives for adjustment to some of its provisions, those adjusted provisions to be returned to the US Senate for consolidation by the Senate before the IIAJA is presented to President Joe Biden for signature.

The passing of the USD 1.2 trillion IIAJA was followed quickly by consideration and some progress on the USD 3.5 trillion 2022 Budget Reconciliation legislation.

As noted in Edition 23, the IIAJA provides for USD 550 billion of new Federal spending on infrastructure, including to upgrade the transmission grid (UTG), to develop recharging infrastructure, to support battery electric vehicle (BEV) use (including by the public school sector), and to support CCS / CCUS. The UTG initiative is particularly important to facilitate the build-out of renewable electrical energy projects across the US.

The World Economic Forum published a helpful summary on August 18, 2021.

It is understood that the US executive is guiding participants to sources of funding, in particular for recharging infrastructure and for the public school BEV buses. This makes perfect sense, because progress can be made quickly in these areas, critically to build the buses (with the Carolinas the likely States in which BEV buses will be built) and to deploy up to 12,000 of them.

The cement, concrete, iron and steel sectors in the US are expecting high demand for their products as a result of infrastructure development under the IIAJA: bridges, tunnels and roads need cement (for the production of concrete) and steel, lots of it.

As noted in the second article in the S2H2 series, the production of cement, iron and steel are the sectors that give rise to the first and second largest CO2 emission levels.

In the US context, a study from the National Academy of Sciences estimated that 8% of CO2 emissions arising globally arise from the production of cement alone, i.e., this estimate does not count GHG emissions arising on extraction, and transportation, of raw materials to produce cement, the transportation of cement from its point of production to the point of concrete preparation, and transportation of concrete from "prep to pour".

In the short-term, NGHGEIs are best used to neutralise the expected spike in GHG emissions, CO2 emissions particularly. The development and implementation of a NGHGEI strategy would be a valid edition to the policy settings tool kit, and in this context could be implemented through the terms on which infrastructure is procured.

On August 11, 2021, it was reported that another bi-partisan bill had been proposed, the Clean Hydrogen Energy Act (CHEA). Low Carbon Pulse will report on the progress of CHEA.

The CHEA may be regarded as key to the achievement of the Hydrogen Earth-shot program: a technology agnostic policy setting seeking to achieve GHG emission free production of hydrogen at USD 1.00 per kg by 2030.

Breakthrough Energy (BE) founder, Mr Bill Gates, continues both as a voice of reason, and as a source of funding. Following the passing of the IIAJA, BE announced that it was working with the US Department of Energy (US DOE), via the BE Catalyst project, to provide up to USD 1.5 billion of funding to accelerate the development of the NZE economy.

As noted in Edition 23 of Low Carbon Pulse, the focus of BE is to provide a platform to accelerate development and deployment of technologies in the following areas: direct air capture and storage (DACS), Green Hydrogen, Long-Duration Energy Storage (LDES) and Sustainable Aviation Fuel (SAF). It is no surprise that BE and DOE have announced that they will work on acceleration of technology projects to develop, in the following order: SAF , Green Hydrogen, DACS and LDES.

Funding of projects in these areas will be coordinated by BE and US DOE. While these areas are not front and centre in the IIAJA, it appears likely that acceleration in these areas will occur. This is a good thing, entirely in keeping with the thinking behind the establishment of BE in the first place (see Edition 19 of Low Carbon Pulse).

In a number of editorials from US publications, it has been noted in the US context that while there has been a reduction GHG emissions arising from the generation of electrical energy in the US over the last 15 years or so, and that the continued progress is being made, this is not enough if the US is to achieve its GHG emission reduction targets in progressing to achieve NZE, let alone to accelerate to NZE. There is an increasing recognition of the need to electrify and to decarbonise on an unprecedented scale.

Microsoft Corporation is leading in the areas in which it does business, and in the decarbonisation of its activities and supply / value chain, in respect of Scope 1, 2 and 3 emissions (see table below).

Microsoft Corporation was founded in 1975 by Mr Bill Gates and, the late, Mr Paul Allen. As noted in Editions 11 and 13 of Low Carbon Pulse, Microsoft is committed to achieving NZE by 2030 and, as noted in Edition 2, to removing from the climate system a mass of CO2-e equal to the mass of GHG emissions that it has emitted since it was founded (zero historical GHG emissions or ZHE) by 2050.

Microsoft is tying its objectives to those of the Paris Agreement (see Articles 2 and 4): first to achieve NZE then to remove GHGs from the atmosphere. Achieving ZHE is an application that Microsoft has added itself.

At the same time that Microsoft committed to NZE and ZHE, Microsoft announced that it was considering the deployment of Fuel Cell Technology (FCT) at its data centres. Edition 13 of Low Carbon Pulse, noted progress on this initiative.

It is understood that considerable progress is being made in respect of this initiative. This is critical given the ever increasing importance and prevalence of data centres, and the electrical energy they require, and the criticality of the assurance as to security of supply of electrical energy.

Set out in the table below is a reminder of each scope of GHG emission.

| SCOPE 1 | SCOPE 2 | SCOPE 3 |

| Direct GHG emissions arising from any activity and source that are controlled or owned by an organization. | IndirectGHG emissions arising from any activity and source not controlled or owned by an organization but used by it. | GHG emissions arising from any activity, not Scope 1 or 2 emissions, but part of the supply chain of that organization. |

UK Hydrogen Strategy (UKH2S) published:

On August 17, 2021, the UK Government published the UKH2S. The arrival of the UKH2S (expected in July 2021) was welcome, taking the author of Low Carbon Pulse by surprise, pleasantly so.

Leaving to one side the pleasant surprise of the publication of UKH2S, given consistency of intent and narrative ahead of publication (including the sibling policy setting, Energy White Paper (EWP), published in December 2020), the UKH2S did not contain any surprises. While some commentators who have characterised an absence of detail as surprising, it is good to have the EWP in mind when reading and reflecting on the UKH2S.

The by-line for the UKH2S is that:

"This strategy sets out the approach to developing a thriving low carbon hydrogen sector in the UK to meet our ambition for 5 GW of low carbon hydrogen production capacity by 2030".

For those familiar with UK Government policy settings, this statement is consistent with the UK Governments Ten Point Plan for a Green Industrial Revolution (published on November 18, 2020) (the Ten Point Plan). Point 2 of the Ten Point Plan driving the Growth of Low Carbon Hydrogen aimed for "5 GW [of] Hydrogen production capacity by 2030 in partnership with industry".

It is fair to say that in some quarters it was hoped that the UKH2S would increase the size of the target aimed to be achieved. As noted in Edition 21 of Low Carbon Pulse, and considered in detail in the July Report on Reports (contained in the Appendix to Edition 23 of Low Carbon Pulse), the All-Party Parliamentary Group urged the UK Government to set more ambitious targets.

For those familiar with the first article in the S2H2 series, Why Hydrogen? Why Now?, and a number of editions of Low Carbon Pulse, the need for the supply and demand side to develop in tandem, with neither being the "chicken or the egg" has long been a theme, as has the idea that to develop supply and demand, Blue and Green Hydrogen are needed.

The UKH2S recognises these supply and demand dynamics in the same way: "Developing a hydrogen economy requires tackling the "chicken and egg" problem growing supply and demand in tandem". Further, the UKH2S recognises that: "When it comes to production, our "twin track" approach capitalises on the UK's potential to produce large quantities of both electrolytic 'green' and CCUS enabled 'blue hydrogen'". (See the EWP for CCUS.)

It is important to note that the UK Government has not been standing still on progress towards the hydrogen economy. As reported in Edition 23 of Low Carbon Pulse, consistent with the Ten Point Plan, and, as can now be seen, aligned with the UKH2S, the UK Government is already laying the foundations through its hydrogen hub / industrial cluster initiatives.

On the day of publication of the UKH2S, one of the five eligible projects announced on July 30, 2021 (see Edition 23 of Low Carbon Pulse, HyNet North West, noted that: "The key now is for the government to build momentum by prioritising projects that are ready for development today". It is difficult to argue with the sentiment, noting however that the sentiment straddles both the EWP and the UKH2S.

Consistent with the approach, and commitment, of the UK Government to long-term partnering with the private-sector, the private sector has been making progress ahead of final policy settings. To get a sense of the level of activity, the following graphic, from MapStand – Location Intelligence is helpful to get a sense of location, and size and shape of activity.

Edition 23 of Low Carbon Pulse provided an overview of the hydrogen hubs and industrial clusters around the UK.

The level of development and definition of these hubs and clusters is a function of the level of development and definition of UK policy settings, and the cohesion across those policy settings.

Each hydrogen hub and industrial cluster is located in an area that is or has been dominated by industry, with activities within its hinterland that give rise to the need for carbon capture (in particular arising from difficult to decarbonise industries, and, to some extent, electrical energy generators using fossil fuels or other carbon intensive fuels), and as such the storge of that carbon, or its storage and use, in proximate storage (depleted oil and gas fields), and the ability to produce hydrogen, (ncluding by virtue of proximate supply of renewable energy and water (Green Hydrogen) or natural gas (Blue Hydrogen), and likely proximate storage for (salt caverns), and use of, the hydrogen produced.

A number of commentators and hydrogen industry participants have questioned the scale and speed of the development of the low carbon production capacity and the "twin-track" approach.

The UKH2S contemplates that a development action plan will be launched in early 2022. Future editions of Low Carbon Pulse will cover these policy settings as they develop further.

On August 9, 2021, publication H2View published an interview with acting Executive Director of Masdar Clean Energy (a leading developer and utility scale renewable energy projects), Mr Fawaz Hadi Salem Ali Al Muharrami. Masdar is celebrating the 15th anniversary of its establishment as a distinct entity, and in this context, the interview is particularly timely.

As reported in Edition 18 of Low Carbon Pulse, Masdar is responsible for the development of a pilot project for the production of Green Hydrogen (and e-kerosene and other sustainable fuels, including sustainable aviation fuel (SAF)). It is expected that Green Hydrogen and SAF will be produced from the pilot project by 2022.

Masdar, Abu Dhabi National Oil Company (ADNOC) and Abu Dhabi Development Holding Company (ADQ) established the Abu Dhabi Hydrogen Alliance (ADHA) earlier in 2021. The ADHA is intended to provide a framework for each organisation to contribute to making the UEA the "trusted leader in low-carbon green and blue hydrogen in emerging international markets". This is bearing fruit.

See: Mubadala, ADNOC and ADQ form alliance to accelerate Abu Dhabi Hydrogen leadership

Edition 23 of Low Carbon Pulse reported on the sale of Blue Ammonia to Itochu by ADNOC and Fertiglobe (a joint venture between ADNOC and OCI NV) to use in the production of fertiliser.

On August 10, 2021, it was reported widely that ADNOC and Fertiglobe had agreed to sell Blue Ammonia to Idemnitsu (leading Japanese headquartered oil corporation) for use in its refining and petrochemical activities.

On August 18, 2021, it was reportedly widely that ADNOC agreed to sell Blue Ammonia to Japan's INPEX (Japan's largest oil and gas exploration and production corporation). It is reported that the CO2 arsing from the production of Blue Hydrogen then combined with nitrogen (producing NH3 molecules) to produce Blue Ammonia is captured and stored in onshore oil fields (in which INPEX is a five percent participant). The Blue Ammonia was produced by Fertiglobe. It is reported that INPEX will use the Blue Ammonia as a fuel for the purposes of electrical energy generation.

The development of the UAE to Japan market for Blue Ammonia reflects the policy settings put in place at both ends of the supply / value change: the UAE has a "twin-track" approach to the production of hydrogen and hydrogen-based fuels, and Japan is agnostic as to the colour of the hydrogen or hydrogen-based fuels imported to displace fuels and feedstocks derived from fossil, and other carbon intensive, fuels and feedstocks.

Note: It is stated frequently that Blue Ammonia emits no carbon or no CO2 on combustion (i.e., on oxidation). This is true: it is a function of NH3 molecules containing no carbon atoms. It is important to note (Ashurst publications do), that on oxidation of ammonia (whatever its colour) N2O arises. N2O is a GHG. This does not lessen the relative benefits of ammonia over other energy carriers, but it is important to understand.

Edition 18 of Low Carbon Pulse reported on the Hyport DUQM Green Hydrogen project in Oman (Hyport DUQM) (under Oman goes Green by Blue). Edition 22 of Low Carbon Pulse reported that Uniper (leading international energy company) has signed a cooperation agreement with the shareholders in Hyport DUQM to develop the business case for the off-take of Green Hydrogen through the negotiation of an exclusive off-take agreement for Green Ammonia and to provide related engineering services.

On August 13, 2021, it was announced that the Oman Ministry of Energy had established an alliance (Hy-Fly) of thirteen public and private sector organisations (including Oman LNG, OQ, BP, Shell and TotalEnergies) to work together to develop initiatives for the purposes of the production, transportation, use and export of clean hydrogen, and clean hydrogen-based fuels.

The establishment of Hy-Fly by the Oman Ministry of Energy is one of the outcomes identified in the Hydrogen Economy Feasibility Study, and it is now part of the Oman Vision 2040.

See: Oman’s hydrogen alliance to drive national hydrogen economy

Edition 14 of Low Carbon Pulse reported on the second round of tenders for renewable projects under National Renewable Energy Program (under Second round solar tender in the Kingdom of Saudi Arabia sees world record low), and the results of the second round of tenders (under which seven projects were awarded), all of which were published on April 8, 2021.

On August 16, 2021, pv magazine, reported that the Sudair solar photovoltaic project (SSPP) had reached financial close, critically, on the basis of a 25 year power purchase agreement. The price under the power purchase agreement is 1.239 cents a KWh or USD 12.139 MWh, the same as the reported bid pricing in early April 2021. (The bid pricing for the SSPP was reported as being the second lowest in the second round of the National Renewable Energy Program.)

The SSPP will be the Kingdom of Saudi Arabia's largest solar photovoltaic project, with 1.5 GW of installed capacity. The SSPP is to be developed by the following leading corporations (in the following shares), ACWA Power (35%), Badeel (35%) and Saudi Aramco (30%), at Sudair Industrial City, about 120 kms from Riyadh. It is remarkable that it has taken a little over months from award to financial close.

See: Financial close for 1.5 GW solar PV project in Saudi Arabia

Edition 18 of Low Carbon Pulse (under Green Hydrogen and Green Ammonia) reported on the announcement of the development of a Green Hydrogen and Green Ammonia facility by Helios Industries within the Khalifa Industrial Zone Abu Dhabi (KIZAD).

On August 16, 2021, it was reported that Helios Industries had contracted with thyssenkrupp to undertake a technical study in respect of an initial production of 20,000 tonnes per annum (tpa) of Green Hydrogen, with production to develop overtime to 200,000 tpa.

As will be apparent from the piece below headed German flagship projects – progress check, thyssenkrupp is the ideal organisation to undertake this work: thyssenkrupp is coordinating one of the three flagship projects critical to the development of the hydrogen economy in Germany - H2Giga: involving the development of large-scale use of electrolysers to electrolyse water using renewable electrical energy to produce Green Hydrogen.

Note: As noted in previous editions of Low Carbon Pulse, across the Gulf Cooperation Council (GCC) countries, there is palpable development of Green Hydrogen and Green Ammonia (and Blue Hydrogen and Ammonia) projects.

Edition 20 of Low Carbon Pulse included a narrative around the highly prospective, world-class resources that exist in the GCC countries (see under Black Gold and Blue and Green Gold, and Oman's aim is true and New petroleum).

As reported in Edition 23 of Low Carbon Pulse, the Executive Director of the International Energy Agency (IEA), Mr Fitoh Birol, regards: "India is a leading country in terms of renewable energy investments … the country has great plans to be a driver of clean energy transitions …". During 2021, this assessment appears to be accurate.

On August 15, 2021, India celebrated the commencement of the 75th year after its founding on August 15, 1947.

On this auspicious day, Indian Prime Minister, Mr Narendra Modi, took the opportunity to announce the National Hydrogen Mission for India (NH2M) in his Independence Day Speech. In the Independence Day Speech, Prime Minister Modi prompted India to give an oath to achieve energy independence before the 100th anniversary of its founding.

Given that India imports 85% of its oil and 53% of its natural gas for domestic energy use, it was not a surprise that energy security for India ran through the narrative of the speech of Prime Minister Modi: the NH2M provides for India to become a global hub for Green Hydrogen production, both for domestic use and for export.

The scale of the ambition is matched by the scale of the plans: from various sources, India plans to install 13.6 GW of renewable electrical energy capacity each year for the next five years, and as such up to 68 GW over that time, with 44.2 GW being utility-scale.

On August 16, 2021, FTI Consulting and Teri published a report (in the South Asia New Energy Series), covering many facets of the development of renewable energy capacity across South Asia.

It is understood that a copy of the report has been provided to the Ministry of New and Renewable Energy (MNRE), among other things, responsible for policy settings in India. The report is well-worth a read, not least because of the focus of what is required ahead of 2030.

As noted below, one of the two more compelling facts reported during Q2 of 2021 is that 5% of the world's electrical energy generation capacity gives rise to 73% of CO2 emissions arising from the generation of electrical energy (see Reducing CO2 emissions by targeting the world's hyper-polluting power plants).

From this report, the ten "worst polluters" were inefficient power plants, using outdated practices and technology, and lower quality coal. These power plants are located in East Asia, Europe and India, with a higher proportion of inefficient coal-fired power stations across these regions.

As noted in Edition 23 of Low Carbon Pulse, UK insurance giant, Prudential, proposes a program to "acquire to retire" coal-fired power stations ahead of the end of their planned life-cycles, critically, before amortisation debt and equity, and, if independent power projects, the term of power purchase agreements under which electrical energy is supplied, typically, to state-owned off-takers of electricity.

On August 13, 2021, Nikkei Asia (under Philippines and Vietnam coal-fired power plants to retire in ADB-led plan), reported that at COP-26, the Asian Development Bank (ADB) intends to announce plans to retire coal-fired powers plants in the Philippines and Vietnam, working with Prudential. As noted in Edition 23 of Low Carbon Pulse, the acquisition and retirement is half the plan, the other half is the development and deployment of new electrical energy generation capacity.

It is understood that the ADB has a short-list of coal-fired power stations this is considered appropriate to close a decade or more before the end of their planned life-cycles. In addition to ADB and Prudential, BlackRock, CitiBank and HSBC have each been mentioned as likely to be involved in the "acquire to retire" program.

It is possible to see a convergence of policy settings here resulting in the cessation of dispatch (in countries with gross wholesale electrical energy markets) and the retirement (in countries with power purchase agreement) of coal-fired electrical energy generation capacity coinciding with new capacity.

As noted in previous editions of Low Carbon Pulse, reverse auctions are used to encourage cessation / retirement, with success in the case of Germany. The challenge with the replication of a reverse auction progress is that it may not result in the retirement of the most inefficient capacity.

As noted in Edition 20 of Low Carbon Pulse, the ASEAN energy ministers met on June 21, 2021, and invited the Japanese Minister for the Ministry of the Economy, Trade and Industry (METI), Mr Hiroshi Kajiyama. At the meeting, Mr Kajiyama announced the USD 10 billion Asian Energy Transition Initiative (AETI). The AETI provides for funding support to ASEAN countries, including to promote the use of gas to power, as a means of displacement coal-fired electrical energy generation.

It is most unlikely that the AETI would be the sole initiative (and it may be resisted in some countries), but it would be an initiative that may be regarded as forming part of other policy settings to retire inefficient coal-fired power generation capacity as quickly as possible with gas-fired electrical energy capacity best suited to integration into current grid infrastructure.

The German Federal Ministry of Education and Research (BMBF) is pivotal in the development of the hydrogen economy in Germany, and further afield for that matter. For example, see Edition 18 of Low Carbon Pulse in respect of the renewable energy resources in Africa under West Africa – untapped potential for hydrogen production). BMBF is key to the implementation of the German National Hydrogen Strategy.

In January 2021, the BMBF launched three flagship projects, and continues to provide funding to them. The three flagship projects are intended to undertake the necessary research and testing to enable the development of the hydrogen economy in Germany.

The three flagship projects are:

Note: For those readers interested in quantum physics, more specifically, the role of Werner Heisenberg in the development of quantum physics, Helgoland, by Carlo Rovelli ("poet of physics"), takes the reader to the tree-less, wind-swept island of Helgoland in the German sector of the North Sea.

In other news from Switzerland, Mammut (leading apparel and equipment supplier) has announced that, as part of its commitment to achieving NZE, it will use only shipping lines with practises that achieve NZE (or lowest carbon) outcomes in respect of its Scope 3 emissions.

Reacting to the Mammut commitment, Climate Change Director, at Pacific Environment (an NGO), Ms Madeline Rose noted: "Mammut's commitment shows that companies have the power to end their maritime freight pollution."

See: Mammut's website and its commitment plan.

On August 17, 2021, the International Energy Agency (IEA) published its Hydrogen in Latin America (H2LA) report. As with all IEA reports, the H2LA report provides a grounding in the key issues and the role that hydrogen may play in decarbonising energy use in Latin America, and the role that Latin America may play globally.

As is the case with most IEA papers, reports and studies, the H2LA provides recommendations for those developing policy settings in Latin American, on this occasion there is six recommendations, as follows:

The August Report on Reports (which will be an Appendix to Edition 26 of Low Carbon Pulse (to be published in September 8, 2021) will contain a summary of the key findings and points made in the H2LA report.

As noted in previous editions of Low Carbon Pulse, a number of Latin American countries have the benefit of renewable resources that will allow the production of hydrogen at scale, in particular Green Hydrogen, and other Green Hydrogen-based fuels. See Editions 10 (under Brazilian government and industry caucus around Green Hydrogen Hub), Edition 13 (under Green Hydrogen (and ammonia and methanol) round-up), Edition 17 (under Chile hot again) and Editions 21 and 23 (under Chile to speed up progress and It is Scotland in Chile).

Most recently, on August 11, 2021, it was announced that the Brazilian state of Rio Grande do Norte has entered into an agreement with "low-carbon energy developer" Enterprize Energy to identify, and to develop, off-shore wind fields and Green Hydrogen and Green Ammonia production.

On August 10, 2021, it was reported widely that Shanghai Electric and Shell China have signed an agreement that will allow the coordination of activities so as to deploy technologies on a timely basis in the context of achievement of the "carbon peak and carbon neutral" outcomes. It is anticipated that this will be a powerful alliance in a rapidly expanding PRC market.

On August 17, 2021, it was reported that the Beijing Municipal Bureau of Economy and Information Technology (MBEIT) released a roadmap routing the development of a hydrogen value chain in Beijing.

Editions 18 and 19 of Low Carbon Pulse reported on the development of hydrogen production facilities in the cities of Baotou and Ordos, Inner Mongolia.

On August 18, 2021, it was reported that the development of renewable electrical energy projects (1.85 GW of solar photovoltaic and 370 MW of wind) will provide the electrical energy to allow the production of up to 66,900 tpa of Green Hydrogen. With construction to commence in October 2021, it expected that first Green Hydrogen will be produced in 2023.

On August 20, 2021, it was reported widely that PRC is to plant 36,000 square kilometres (an area that is larger than the size of Belgium) of new forest a year until 2025. By the end of 2025, over 24% of land mass in PRC will be forested. This goes beyond policy setting of preserving and returning land to ensure that at least 30% of land mass is unused for human activities (see Edition 14 of Low Carbon Pulse).

Edition 23 of Low Carbon Pulse reported on a comprehensive article in Oil Price (under Russia Ramps Up Its Hydrogen Energy Ambitions), in which various narrative strains that have emerged over the last few months (certainly starting in May 2021) are pulled together.

On August 9, 2021, it was reported widely that framework plans for the development of the hydrogen economy in Russia (including for the export of hydrogen) have been approved, in principle, by the Russian Prime Minister, Mr Mikhail Mishustin. This is effectively a hydrogen strategy.

It is understood that the framework plans contemplate the development of three clusters for the production of hydrogen: in the Northwest sector of Russia (to provide hydrogen to European countries), in the Eastern sector of Russia (to provide hydrogen to Asian countries, including into North Asia) and in the Arctic sector.

As might be expected, the production of Blue Hydrogen (using natural gas as the feedstock, and steam methane reforming and CCS / CCUS technologies) will be the focus of each cluster, at least until the latter part of the current decade. It is contemplated also that coal may be used as a feedstock for hydrogen production.

Russia has vast resources that will enable it to be a key player in the emerging markets for hydrogen and hydrogen-based fuels and feedstocks. As is the case with all oil and gas companies globally, Russian oil and gas companies recognise the need to transition to low or no carbon energy carriers.

The 2021 Report does not address bio-energy in the same level of detail as any of the following.

The 2021 Report recognises bio-energy as one of the means of carbon dioxide removal (CDR) on the basis that bio-energy being derived with carbon capture and storage (BECCS). BECCS is recognised is one of a number of means of achieving CDR along with afforestation, DACS, enhanced terrestrial weathering, ocean alkalinisation and ocean fertilisation, soil carbon sequestration and wet-land restoration.

For further detail on CDR (including the means of achieving enhanced terrestrial weathering, ocean alkalinisation and ocean fertilisation, soil carbon sequestration and wet-land restoration), see Chapter 5, Section 5.6 of the 2021 Report.

CDR is not an instant solution in global terms (as outlined in Edition 24 it takes time), nor is BECCS. For BECCS to make a contribution to a reduction in GHG emissions, it must displace another electrical energy source or energy carrier source, and, in any event, it must result in a carbon neutral outcome (rather than a carbon removal outcome) so as not to give rise to an increase in GHG emissions. The effectiveness of BECCS at a global level is more likely than not to be to achieve carbon neutrality rather than to remove carbon.

The key findings in the 2021 Report in the realm of Blue Carbon are:

"It is virtually certain that the global upper ocean (0-700 metres) has warmed since the 1970s and extremely likely that human influence is the main driver. It is virtually certain that human-caused CO2 emissions are the main driver of current global acidification of the surface of open ocean. There is high confidence that oxygen levels have dropped in many upper ocean regions since the mid-20th century … "

This is taken from that Summary of Policymakers (SPM) contained in the 2021 Report. (The SPM is the part of the 2021 Report from which it is possible to cite and to quote.)

The key findings of the 2021 Report support the perspective that, with the exception of the restoration and planting of mangrove swamps and other flora close to oceans and waterways, as yet the science tends to support a Socratic approach – do no harm. In fact, it is probably fair to displace "do no harm" with "do nothing at all" approach. As noted in the 2021 Report, it is critical to avoid activities that may increase the upper ocean temperature or that may increase acidification or reduce the level of oxygenation in the oceans.

On August 20, 2021, it was reported widely that on September 8, 2021, Orca, a new direct air capture and storge facility, will commence in Iceland. Orca, owned by Climeworks, will capture up to 4,000 tpa of CO2 from the atmosphere, and store the captured CO2 underground.

See: The rapid construction of Climeworks' new direct air capture and storage plant Orca has started

On August 21, 2021, the Australian Broadcast Corporation news developed a news item from a study that is a couple of years old from The Australia Institute (a think tank known for conducting a range of research). The news item is intended to frame the "technology not taxes" policy setting mind-set of the current Australian Federal Government. The news time grabs the attention with the headline that: "The Australian Institute says that about $4 billion of taxpayer money has been spent on CCS" since 2023.

The 2021 Report (and each of the IEA, IRENA and BloombergNEF reports) contemplates the use of CCS, and that its use is critical to achieving NZE, each noting that use of CCS is a less assured policy setting than others.

Leaving to one side the purpose of the ABC news item, it is important to note that what matters is that CCS / CCUS is used and that it is used promptly, with its use to be perfected over time. It is not a question of renewable electrical energy versus CCS / CCUS, it is a matter of the deployment of both renewable electrical energy and CCS / CCUS promptly, and its perfection as soon as practicable.

See: As carbon capture, storage spending nears $4b, what are the options for heavy industry?

On August 21, 2021, it was reported that researchers in Switzerland had released a study containing encouraging findings about the use of DACS as a means of CCS. CO2 capture was undertaken in Chile, Greece, Iceland, Jordan, Mexico, Norway, Spain and Switzerland for the purpose of the study. The key finding is that up to 97% of CO2 in the atmosphere could be captured direct-from-air using DACS technologies.

While the study may be regarded as stating the obvious in parts ("The use of [DACS] technology only makes sense if [the emissions arising from the use of the technology] are significantly lower than the amounts of CO2 it helps to [capture and] store"), it is well-worth a read.

On August 12, 2021, Australia's National Science Agency, the Commonwealth Scientific and Industrial Research Organisation (CSIRO), published its CO2 Utilisation Roadmap (CUR). For the author of Low Carbon Pulse, this is timely, and, as one has come to expect, given the sustained excellence of the CSIRO, the CUR is excellent.

The CUR will be considered in detail in the August Report on Reports, which will be included as the Appendix to Edition 26 or Edition 27 of Low Carbon Pulse (to be published on September 8, 2021 or September 22, 2021).

On August 9, 2021, it was widely reported that AGL Energy Limited (AGL), one of Australia's three large integrated energy companies, is to develop the world's largest Big Battery with the development of a "grid forming" battery of 250 MW to be located at Torrens Island, Adelaide, South Australia (GFB). (As noted below, the title of world's largest Big Battery is unlikely to be held for long.)

This is a continuation of AGL's response to energy transition with big battery capacity of up to 850 MW to be developed and owned and controlled by it, to add to its established business model to contract for capacity in Big Batteries owned by other corporations, including in respect of Wandoan and two Big Batteries being developed by Maoneng (see Edition 21 of Low Carbon Pulse).

Initially, the GFB will have one hour of storage capacity (250 MW / 250 MWh). Eventually, the GFB will have four hours of storage (250 MW / 1,000 MWh). The development of the GFB is to take place at the AGL's Torrens Island Gas Fired Power Station (TGFPS) as TGFPS is retired over time. Wartsila (global leading energy and battery system corporation based in Finland) is to supply the technology and construct and install the GFB, and with SMA Solar Technology (leading German corporation) to supply the inverters.

As noted in Edition 21 of Low Carbon Pulse, BESSs are able to provide virtual synchronous generation capacity.

See: AGL invests $180 million in Torrens Island grid-scale battery

On August 16, 2021, Energy-Storage.news reported on a proposal to develop a 150 MW / 600 MWh BESS as part of a "state-of-the-art clean energy underground highway" to transit green electrons from Upstate New York to The Big (Green) Apple.

The background to the proposed project is the commitment of New York State to source 70% of electrical energy from renewable electrical energy sources by 2030. Upstate New York has good renewable energy resources that would support the proposed project.

On August 22, 2021, CleanTechnica published a piece outlining a 1,500 MW / 6,000 MWh new energy storage facility proposed by Vistra. The proposed project would dwarf the 400 MW / 1,600 MWh Moss Landing Energy Storage Project (developed by Vistra Zero).

Edition 19 of Low Carbon Pulse reported on the plans of Plug Power to develop a Green Hydrogen production facility in Georgia, US. On August 10, 2021, it was reported that Plug Power had "broken ground" commencing construction of the facility that will produce 15 tonnes of liquid hydrogen each day.

As noted in previous editions of Low Carbon Pulse, while the capacity of any single Green Hydrogen production facility may not appear significant, the development of production facilities are significant because of the number of them being developed, the fact that they are being developed to match supply to demand for the Green Hydrogen on an incremental market-by-market basis, and that the electrical energy used to produce the Green Hydrogen is from a renewable resource.

See: Plug Power breaks ground on green hydrogen production plant in Georgia

Edition 16 of Low Carbon Pulse reported on Province Resources Limited's HyEnergy Project in Western Australia. On August 11, 2021, it was reported widely that Global Energy Ventures Ltd and Total Eren have signed a memorandum of understanding with Province Resources Limited in respect of the possible export of Green Hydrogen from the HyEnergy Project.

See: Global Energy Ventures hails MoU with HyEnergy project

On August 11, 2021, it was reported widely that an application had been made to develop the first hydrogen fuel hub (HFH) in Manchester, in the Trafford area of the city, at the Trafford Low Carbon Energy Park. The HFH will produce and store Green Hydrogen. The plans indicate that the HFH will have capacity of 200 MW, making it the largest contemplated in the UK to date.

See: Trafford Green Hydrogen advances 200 MW renewable fuel hub in UK

Previous editions of Low Carbon Pulse have reported on the activities of Everfuel (leading Scandinavian energy carrier mobility corporation) as one of the most active and forward thinking Green Hydrogen entities in Northern Europe, including to outline the development of hydrogen refuelling infrastructure (HRI) across Scandinavia (see Edition 18 of Low Carbon Pulse), and production partnerships with Greenstat ASA (see Edition 21 of Low Carbon Pulse).

On August 12, 2021, it was reported that Everfuel is to develop the HySynergy Phase I 20 MW electrolyser Green Hydrogen production facility at Fredericia, Denmark. It is understood that Phase II contemplated a 300 MW Green Hydrogen production facility. This initiative builds on, and enhances, the Everfuel business model

On August 12, 2021, it was announced that NEL Hydrogen US (part of the Norwegian based NEL ASA Group, leading electrolyser technology provider) is to supply a PEM electrolyser funded by the US DOE to produce hydrogen for use at a nuclear power plant. The PEM electrolyser is to be installed at the Exelon Generation Nine Mile Point nuclear power plant in Oswego, New York State, located on Lake Ontario.

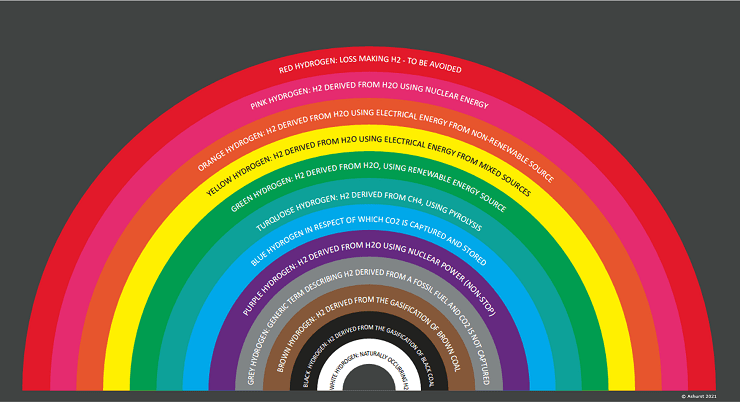

It is not clear as yet whether the hydrogen will produce hydrogen using electrical energy from the plant (Pink Hydrogen) or steam from the plant (Purple Hydrogen).

By way of background information, attached is a link:

As a point of contrast (ladder and rainbow), and for immediate reference, set out below is the Ashurst Hydrogen Rainbow:

The Ashurst Hydrogen Rainbow (a creation of the author of Low Carbon Pulse), is intended to provide an aide memoire to the reader. It is noted that the author of Low Carbon Pulse took liberties with both the colour coding of hydrogen and the spectrum: adding Red Hydrogen (at the top of the Rainbow) to represent the difficulty of making a return on any early stage clean or low hydrogen project, and adding Grey, Brown, Black and White (at the bottom of the Rainbow) for completeness of the colours that are used to describe hydrogen.

On August 13, 2021, the PCCA and Howard Energy Partners announced plans to develop a carbon-neutral hydrogen production facility at the Javelina plant. These plans are the subject of a memorandum of understanding under which the Javelina plant will be converted to produce hydrogen, and on conversion, supply six local refineries using pipeline infrastructure.

As will be apparent, there is a lot going on in Norway (and Denmark, Finland and Sweden for that matter). In addition to the news items noted above, attached is a link to a bulletin from SINTEF Energy Research, providing updates, among other things, on CCS / CCUS and waste to energy.

On August 16, 2021, it was reported that a P2X Solutions is to develop a 20 MW Green Hydrogen production facility (PSP). It is reported that the Green Hydrogen produced will be supplied to industrial users.

Interestingly, it is reported that Green Oxygen will be used as a by-product. The derivation and use of oxygen has not tended to be the norm in the context of P2X narratives, but it may be expected that it will become part of the narrative increasingly.

See: First green hydrogen production plant in Harjavalta

Edition 19 of Low Carbon Pulse reported on Bakken Energy and Mitsubishi Power Americas Inc's strategic partnership to create a clean hydrogen hub in North Dakota, US.

On August 19, 2021, HydrogenCentral, reported (under Bakken Energy to Purchased Dakota Synfuels Plant and Convert to Blue Hydrogen, $ 2 B Hydrogen Hub Project) that Bakken Energy had agreed terms with Basin Electric Power Corporation to purchase the gas assets of the Dakota Gasification Company, including its Synfuels facility.

It is reported that Synfuels facility will be expanded and repurposed, and that it will incorporate advanced autothermal reforming (ATR) technology, rather than steam methane reforming (SMR) technology, to increase and to maximise the capture of CO2 arising during the production of clean hydrogen (being hydrogen using carbon intensive feedstock that is then reformed).

The ATR technology to be deployed is reported as capturing of 95% of carbon emissions arising. It is hoped that that Bakken will seek to address the 5% not covered by capture through a sequestration strategy.

On August 19, 2021, Norway's Maersk (the world's largest container shipping company) announced that it had contracted with Denmark's European Energy (and its subsidiary REIntegrate) for the development of an e-methanol production facility (e-mpf), and supply from it.

The Practical: The e-methanol produced from the e-mpf (stated to be up to 10,000 tpa) will be:

derived from biogenic CO2 (i.e., CO2 captured from renewable organic feedstock); and

supplied to Maersk to power and to propel "the world's first container vessel operating on carbon neutral fuel".

This initiative keeps Maersk on schedule to have: "the world's first container vessel operated on carbon neutral methanol on the water by 2023".

The Theory: As noted in previous editions of Low Carbon Pulse (most recently in Edition 22 of Low Carbon Pulse, under Why methanol?), while the oxidation of e-methanol (and any other bio-organic sourced fuel) is not CO2 free, "the theory is that the CO2 that arises will be absorbed into a renewable resource, with the continued growth in that renewable resource providing a carbon neutral outcome". This is the theory, noting that the science is still more theoretical than firm.

From the other end of the "growth-to-emission cycle", the US Environmental Protection Agency has stated that CO2 emissions arising from biogenic sources are "emissions that come from natural sources".

Previous editions of Low Carbon Pulse have reported on the development of the Hydrogen Park South Australia (HyP SA).

On August 20, 2021, it was reported that HyP SA is closing on the final stages of commissioning of the hydrogen production facility, and will commence the supply of hydrogen to Whyalla, South Australia, shortly.

See: Hydrogen Park South Australia website

On August 21, 2021, Naftogaz and RWE signed a memorandum of understanding to work together to identify opportunities in the Green Hydrogen market, principally developing Green Hydrogen and Green Hydrogen-based fuels (including Green Ammonia) production facilities in Ukraine and supply in Germany and Europe more broadly.

See: Naftogaz and RWE sign memorandum of understanding on hydrogen

Recent editions of Low Carbon Pulse have noted moves by a number of alumina and aluminium producers to green their production processes. On August 11, 2021, Australia's largest aluminium smelter owner, Tomago Aluminium, announced that it is to procure electrical energy from renewable sources from 2028. This decision will displace the use of electrical energy currently sourced from coal-fired sources.

On August 16, 2021, Australian headquartered Bluescope Steel Limited (BSL) announced that it is committed to NZE for its Scope 1 and Scope 2 emissions. BSL is to achieve this NZE commitment using renewable electrical energy, and Green Hydrogen, rather natural gas (CH4), whether alone or blended with hydrogen.

As has been reported in a number of editions of Low Carbon Pulse, a number of steel makers are moving to sourcing high-temperature heat using CH4 (rather than coal), with the intention to move to Blue or Green Hydrogen overtime, including using blending. BSL is not taking this approach, and as such the transition to Green Steel production may take longer as the supply side of the Green Hydrogen industry develops.

In any event, BSL recognises that achievement of its NZE commitment is not going to be easy, and that reductions in GHG emissions will occur, gather pace, after 2030.

See: BlueScope to Pursue Net Zero by 2050

See: The world’s first fossil-free steel ready for delivery

A previous edition of Low Carbon Pulse reported on the establishment of the first hydrogen hub in Canada, at Edmonton.

On August 13, 2021, plans for a second hydrogen hub were announced in Southeast Alberta (SEAH2H). For the purposes of assessing whether and, if so, how to develop the SEAH2H, the Southeast Alberta Hydrogen Task Force has been established.

Over the last quarter or so, two facts have resonated more than others, as follows:

In the context of reducing GHG emissions at a greater rate than currently contemplated, certainly at a rate greater than combined NDCs contemplate, policy settings need to progress on a basis largely informed by these statistics. In this context, the built urban environment is a pressing an area for action to reduce GHG emissions as any other. Future editions of Low Carbon Pulse will include a feature on policy settings in this area.

Note: Edition 26 of Low Carbon Pulse will include a feature on giga-factories - those recently opened and those planned. Given recent activity, a feature of this kind had been planned for this Edition, but space became a premium (seeking to limit each edition of Low Carbon Pulse to 15 pages of narrative / 13,000 words).

On August 16, 2021, it was reported widely that the Green Investment Group Limited (GIG) and TotalEnergies has been granted an electricity business licence (EBL) from the Ministry of Trade, Industry and Energy. The grant of an EPL allows the development, and exclusive basis, of the first phase (504 MW) of the three phase 1.5 GW off-shore floating wind field project off Ulsan, South Korea.

See: GIG & TotalEnergies Obtain EBL for Korea’s First Floating Offshore Wind Farm

Edition 18 of Low Carbon Pulse reported on the arrangements relating to the development of the Port of Cromarty as a hydrogen hub. On July 23, 2021, it was reported that Cromarty Firth has been identified as the ideal location for a 35 MW, Green Hydrogen production facility (see Edition 22 of Low Carbon Pulse).

As reported in Edition 22 of Low Carbon Pulse, the ScotWind Leasing Scheme auction process is going to result in the award of leases to allow the development of offshore wind fields, fixed bottom and floating. In this context, there is going to be a need for the provision, on-shore to off-shore, of manufacture and fabrication, and installation, service industry development. The need is recognised, how best to satisfy the need is now the focus of attention.

On 19 August, 2021, an independent report prepared for the Scottish Offshore Wind Council (SOWEC), chaired by Sir Jim McDonald, has come out strongly in favour of the development of a floating wind port cluster in the North of Scotland (see Scottish Offshore Wind Strategic Investment Assessment: An Independent report to the Scottish Offshore Wind Energy Council), with Cromarty Firth the most suitable area in Scotland for platform manufacture and fabrication.

Within the Cromarty Firth and Moray Firth area, the two ports of Invergordon and Nigg (in East Ross) are regarded as being suitable for manufacture and fabrication locations, with their use for this purpose requiring significant increased capacity at each port. Other ports that may expect to gain from the next wave of off-shore wind field development are Aberdeen, Dundee and Leith, and Hunterston (Ayrshire), and Loch Kishorn (Wester Ross).

Note: The news items on Cromarty Firth could be been included in the usual Ports and Shipping Forecast section, is included under Wind round-up for convenience.

On August 9, 2021, Pollution Solutions on line published an article outlining the potential for hybrid solar and bio-energy projects in Pakistan using gasification technology to derive biogas and biomethane.

On August 21, 2021, electrical energy dispatched from solar sources exceeded the electrical energy dispatched from coal fired power stations across the national electricity market in Australia.

After a flood of new items on land transport in recent editions of Low Carbon Pulse, the two news cycle for this Edition 25 of Low Carbon Pulse has seen far fewer news items, and they will be included in Edition 26 of Low Carbon Pulse, noting however that some land transport news items are included elsewhere within this Edition 25.

Edition 26 of Low Carbon Pulse will include the promised feature on development of NZE initiatives in the Aviation and Airports sector.

As noted above, at the end of future editions of Low Carbon Pulse, reports that have been reviewed for the purpose of that edition of Low Carbon Pulse will be listed, by organisation, title / subject matter, and link.

| ORGANISATION | TITLE / SUBJECT MATTER |

| International Energy Agency | Net Zero by 2050 – A Roadmap for Global Energy Sector |

| International Energy Agency | Hydrogen in Latin America |

| International Renewable Energy Agency or IRENA | World Energy Transitions Outlook |

| Wood Mackenzie | How to scale up carbon capture and storage |

| BloombergyNEF | New Energy Outlook, 2021 |

| S&P Global Platts | Platts Global Integrated Energy Model – Strategic Planning for a world in transition. |

| FTI Consulting and Teri | South Asia New Energy Series |

| Intergovernmental Panel on Climate Change (IPCC) | Sixth Assessment Report – Climate Change 2021, The Physical Science Basis (2021 Report) |

| Commonwealth Scientific and Industrial Research Organisation | CO2 Utilisation Roadmap |

The author of (and researcher for) Low Carbon Pulse is Michael Harrison.

The information provided is not intended to be a comprehensive review of all developments in the law and practice, or to cover all aspects of those referred to.

Readers should take legal advice before applying it to specific issues or transactions.

Sign-up to select your areas of interest

Sign-up